How to Structure Financing for Property Flipping Projects in 2025

Property flipping as an investment strategy

Property flipping is a dynamic investment strategy built around a straightforward cycle: buy undervalued properties, renovate them to increase their worth, and sell quickly at a profit. This approach allows investors to generate meaningful returns over much shorter cycles than most traditional real estate strategies require.

That said, success in property flipping does not rest on finding the right property alone. The strength of the underlying financing structure can make or break a project — it is not a secondary consideration.

In this article, we examine the main financing options available for flipping projects, the steps involved in securing them, the requirements lenders impose, and the financial strategies to keep in mind at every stage from acquisition to sale.

IMPORTANT DISCLAIMER: The content of this article is for informational purposes only. The information provided does not constitute financial, legal, tax, or investment advice. The strategies, data, and figures regarding returns mentioned are estimates based on general market conditions and may vary significantly depending on the particular circumstances of each investor, property, location, and economic environment. The author and publisher of this content assume no responsibility for decisions readers may make based on this information.

Table of Contents

- Understanding Property Flipping

- Financing for Property Flipping: Options and Alternatives

- How to Finance Property Flipping

- Property Flipping Financing Requirements

- Conclusion

- Frequently Asked Questions (FAQ)

Key points about financing for property flipping:

- The financing structure you choose will directly determine the overall profitability of the project. Working with independent expert advisors and evaluating all available options is essential.

- Multiple specialised alternatives exist: traditional bank loans, bridge loans, crowdfunding, and private loans — each suited to different investor profiles and project types.

- A detailed business plan with solid market analysis and financial projections significantly improves your chances of securing favourable financing.

- The 75% rule is the standard benchmark for assessing flipping opportunities and ensuring adequate profit margins.

- Keeping a contingency fund of 10–15% of the total budget is critical for handling unexpected costs without putting the project at risk.

Understanding Property Flipping

What exactly is property flipping?

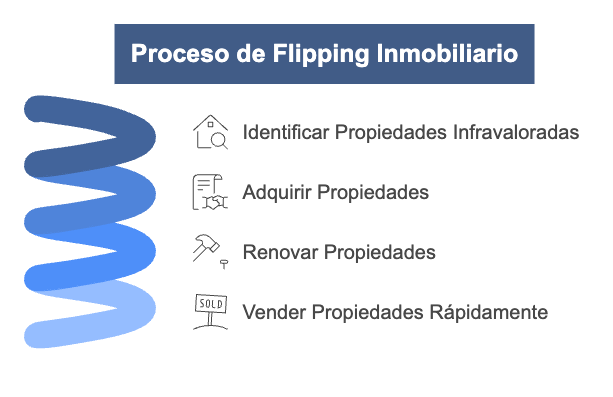

Property flipping involves acquiring properties well below their market value, renovating them strategically to increase their appeal and value, and selling quickly to generate a strong return. Unlike rental strategies, which target long-term income, flipping is defined by:

- Short investment cycles (typically 6–12 months)

- A focus on aesthetic and functional renovation

- A deliberate search for undervalued properties with revaluation potential

- A target of a quick sale at a meaningful profit margin

The key to making this work is buying with enough margin built in to cover all associated costs — acquisition, renovation, holding costs, taxes, and financing — and still come out with an attractive profit. This strategy has established itself as one of the most dynamic approaches to real estate investment in the Spanish market, as we explore in our complete guide to property flipping.

The critical importance of financing

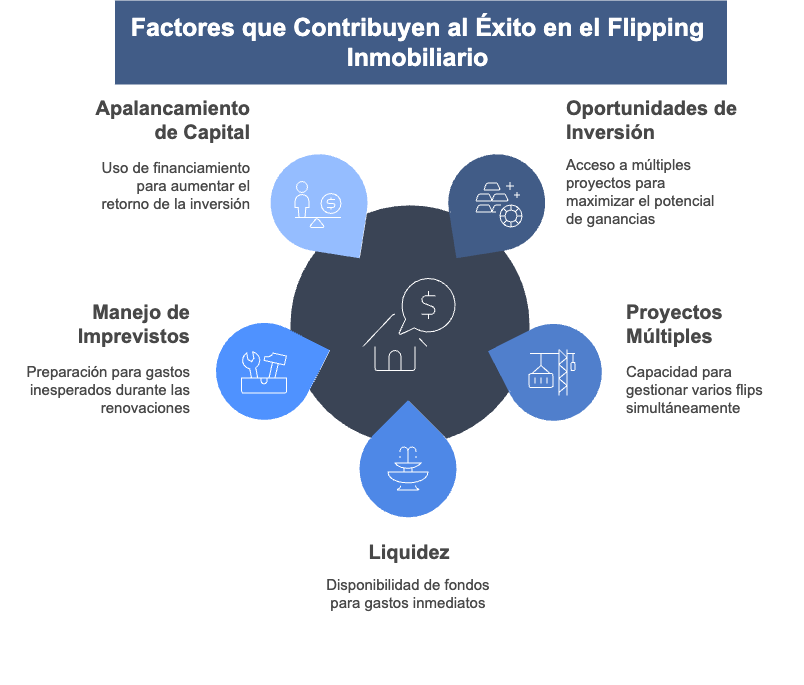

Solid financing for property flipping matters for several interconnected reasons:

- It opens up more investment opportunities

- It makes running multiple projects simultaneously feasible

- It ensures sufficient liquidity throughout the entire process

- It provides a buffer for unexpected costs during the renovation phase

- It maximises the return on equity through leverage

Even the most promising project can stall — or fail entirely — if the financial structure is not solid. The difference between occasional investors and consistently successful professionals is largely their ability to structure financing well.

Financing for Property Flipping: Options and Alternatives

Several financing options are available for property flipping projects in the Spanish market, each with its own trade-offs.

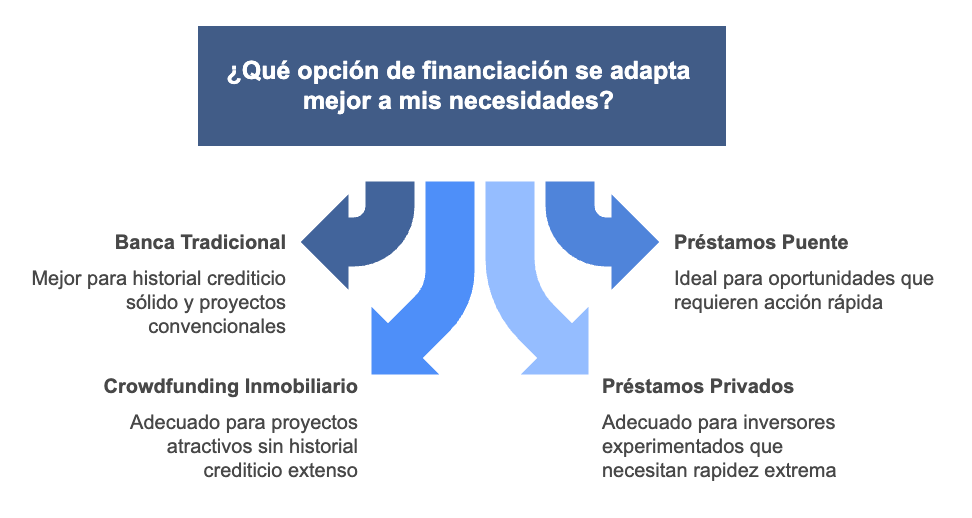

Traditional banking

Bank financing for flipping projects can take two main forms:

-

Conventional mortgages: Offer stable conditions and long terms, but approval processes are slow and requirements are strict.

-

Developer loans: Specifically designed for real estate projects, with phased disbursements as construction progresses. They typically cover 50–70% of total costs. For a deeper look at how these loans work, see our guide on developer loans.

Advantages:

- Stable, predictable financing conditions

- Institutional backing and security

- Ability to finance large amounts

Disadvantages:

- Slow approval (typically 1–3 months)

- Demanding documentary and solvency requirements

- Limited flexibility for non-standard projects

Bridge loans

Bridge loans are short-term instruments designed to bridge the gap between acquiring a property and refinancing or selling it:

Advantages:

- Fast approval (1–3 weeks)

- Assessment focused on property value and potential, not just the borrower's profile

- Terms aligned to the flipping cycle (6–24 months)

Disadvantages:

- Less favourable terms than traditional bank financing

- May require additional security

- Shorter terms create more time pressure to complete the project

Bridge loans are particularly useful when an opportunity demands a quick decision, or when the investor does not fully meet standard bank lending criteria.

Real estate crowdfunding

Real estate crowdfunding has grown significantly as a financing channel for flipping projects:

Advantages:

- Access to capital without meeting strict bank requirements

- Can finance 30–70% of the project

- Fully digital, streamlined processes

Disadvantages:

- Less favourable terms than bank financing

- Projects need to appeal to multiple investors

- Some platforms impose restrictions on how the project can evolve

Crowdfunding platforms assess primarily the project's viability and return potential, which can open doors for investors who lack an extensive credit history.

Private loans

Private investor loans offer a flexible alternative for property flipping:

Advantages:

- Very fast approval (sometimes within days)

- Flexible terms and conditions

- Assessment based almost entirely on property value rather than the borrower's credit profile

Disadvantages:

- Generally less favourable terms

- Often require additional personal guarantees

- Shorter terms increase execution pressure

These loans suit experienced investors who need to move extremely quickly or who do not qualify for traditional financing.

| Financing Option | Main Advantage | Main Disadvantage |

|---|---|---|

| Traditional banking | Stable and secure conditions | Slow approval |

| Conventional mortgage | Long terms | Elevated requirements |

| Developer loan | Phased disbursements | Partial financing (50–70%) |

| Bridge loan | Fast approval (1–3 weeks) | Short terms (6–24 months) |

| Real estate crowdfunding | Agile and digitalized processes | Less flexibility |

| Private loan | High flexibility | Less favourable terms |

Looking for financing for a property flipping project? Contact us with no obligation. Our team will respond within 24 hours to assess what options are available for your situation.

How to Finance Property Flipping

Successfully financing a property flipping project requires a structured approach from the outset.

1. Assess the viability of the project

Before approaching any lender, you need to:

- Analyse the local market: Study prices, demand, and typical sale speeds in the target area.

- Estimate renovation costs accurately: Get detailed quotes from contractors before committing.

- Calculate the estimated after-renovation value (ARV): Base this on recent comparable sales, not optimistic assumptions.

- Account for all associated costs: Taxes, insurance, holding costs.

A rigorous assessment tells you how much financing you need and whether the project has the potential to deliver the return you're targeting. To maximise that return, renovation selection is critical — see our article on the 7 renovations that maximise ROI in property flipping.

2. Apply the 75% rule to evaluate opportunities

In professional property flipping, the 75% rule is the standard profitability check:

Purchase price + Associated costs + Renovation cost ≤ 75% of the Post-Renovation Value

This 25% safety margin covers unexpected costs, financing charges, and your target profit. Applying it correctly:

- Determine the post-renovation value (PRV) by analysing comparable renovated properties nearby.

- Calculate the maximum total price (MTP) by multiplying the PRV by 0.75.

- Estimate all costs — renovation, transaction costs, financing, and a contingency buffer.

- Set your maximum purchase price by subtracting all costs from the MTP.

This financial discipline is what keeps projects viable and profit margins intact.

3. Prepare a detailed business plan

A solid business plan should cover:

- Market analysis: Local real estate trends and likely demand.

- Acquisition strategy: How you identify and secure undervalued properties.

- Renovation plan: Scope, schedule, and itemised budget.

- Financial projections: Cash flows, expected ROI, and sensitivity analysis.

- Exit strategy: Your marketing and sales plan.

- Risk analysis: Potential problems and how you'll address them.

This document is your primary tool for convincing lenders that your project is viable. Include a clear section on risk mitigation — a topic we cover in depth in our article on how to manage risk in property flipping operations.

4. Diversify financing sources

Combining different financing sources is an increasingly common approach among experienced investors, and for good reason:

- Staged financing: Match different instruments to different project phases — acquisition, renovation, sale.

- Hybrid financing: Use a bank loan for the purchase and private financing for the renovation works.

- Co-investment: Partner with other investors to share both the capital requirement and the risk.

This approach not only reduces the overall cost of capital but also limits dependence on any single lender — itself a meaningful form of risk management.

Property Flipping Financing Requirements

Understanding what lenders look for puts you in a much stronger position when approaching them.

Experience and track record

Flipping demands specific skills, and lenders take note:

- History of completed projects: Demonstrable experience typically leads to better terms.

- A strong technical team: Working with trusted architects, quantity surveyors, and contractors strengthens any application.

- Local market knowledge: Specialisation in specific areas or property types is viewed positively.

Investors without prior experience can partially offset this by partnering with seasoned professionals or presenting a strong technical team.

Financial capacity and credit profile

- Clean credit history: A solid CIRBE (Bank of Spain Risk Information Centre) record is essential.

- Debt ratio: Most lenders prefer total debt obligations below 40–50% of income.

- Financial stability: Evidence of stable income sufficient to handle contingencies.

- Available equity: Most lenders require 20–40% of total project costs to come from the borrower's own funds.

The strength of your financial profile has a direct bearing on the terms you can negotiate.

Analysis of the specific project

Lenders specialising in flipping focus primarily on:

- Location and market potential: Areas with consistent demand and good appreciation prospects.

- Projected profit margin: Confirmed by applying the 75% rule.

- Technical feasibility: An honest assessment of renovation complexity.

- Exit strategy: A realistic sales plan with credible alternatives if conditions change.

These factors often carry more weight than the borrower's personal profile, especially with alternative lenders such as bridge loan providers and private capital funds.

Conclusion

Financing for property flipping is one of the pillars on which the strategy rests. As this article shows, the market now offers a range of specialised options, each with characteristics that can be matched to the specific needs of a project and its investor.

Optimising the financial structure means understanding the distinctive features of property flipping: its short cycles, the way liquidity needs shift at each project phase, and the importance of having headroom when the unexpected happens. This is not simply about raising money — it is about designing the right structure for each specific situation.

To maximise your chances of success:

- Build relationships with multiple financing sources — never rely on just one.

- Structure financing by phase, tailored to what each stage actually needs.

- Always hold financial reserves for contingencies (at least 10–15% of the total budget).

- Apply rigorous financial criteria to every deal, anchored to the 75% rule.

- Negotiate all terms, not just the interest rate — repayment schedules, grace periods, and flexibility matter just as much.

Property flipping can generate very attractive returns when approached with proper preparation. The difference between ordinary projects and highly profitable ones lies precisely in the financial structure that underpins each transaction.

Planning your next real estate development or looking for financing for a property flipping project? Contact us today for a free initial assessment. Our team will get back to you within 24 hours with a clear view of the financing options available for your specific situation.

Frequently Asked Questions (FAQ)

What type of property is ideal for a property flipping project from a financial perspective?

The best flipping properties combine several characteristics: an acquisition price well below market value (20–30% below), renovation requirements that are primarily cosmetic or functional rather than structural, a location with strong demand and good sales turnover, and a manageable size that keeps financing accessible. The optimal balance between purchase price, renovation budget, and achievable sale price is the deciding factor — more so than any particular property type.

What are the main requirements for property flipping financing?

Requirements vary by lender type, but typically include: an equity contribution of 20–40% of project costs; a detailed business plan with market analysis and financial projections; a professional valuation of the property before and after the planned renovation; an itemised construction budget; and a clear exit or sales strategy. For investors without prior experience, many lenders place particular emphasis on the quality of the technical team — architects, quantity surveyors, and a reputable contractor.

How does the financial structure affect the final profitability of the project?

The financing structure has a direct impact on returns through several channels: total financing costs reduce the net profit; the level of leverage amplifies equity returns when the project succeeds; flexible terms allow the project to absorb surprises without triggering costly penalties; and loan duration creates the time pressure to complete and sell. A well-designed financial structure can improve the return on equity by 40–60% compared with a poorly structured equivalent for the same project.

How can different financing sources be combined in a flipping project?

An effective mixed approach might work as follows: use traditional bank financing for the initial acquisition, taking advantage of its more stable conditions; layer in bridge loans or private capital for the renovation phase, where speed and flexibility matter more; and keep a credit line available as a backstop for unexpected costs. The key is making sure the terms of different facilities are compatible — particularly regarding security arrangements and repayment priority.

What strategies exist to mitigate financial risks in property flipping?

The most effective risk management strategies include: holding a contingency reserve of at least 15% of the total budget; structuring financing with grace periods or extended terms to create a time buffer; working with multiple lenders rather than depending on one; taking out specialist insurance for renovation projects (all-risks construction, public liability); implementing rigorous cost-tracking with weekly reviews; and having a credible fallback plan — such as renting the property temporarily — if market conditions make an immediate sale difficult. Applied consistently, these measures turn financial risk management into a genuine competitive strength.