Is the Developer Loan the Best Option for Your Real Estate Project?

The developer loan has become a decisive factor in the success of any real estate project in today's competitive Spanish market. Having analysed hundreds of financing transactions over more than 20 years advising developers, at GrupInversor we have found that this financial instrument stands out for its flexibility and its ability to adapt to the specific needs of each development.

Unlike other financing products, the developer loan is designed to support every critical phase of your real estate project — from the initial land acquisition through to the handover of completed units. Yet, surprisingly, many professionals in the sector still fail to fully leverage its advantages or to negotiate the best possible terms.

This guide covers everything you need to know about the developer loan: how it works, what it costs, what lenders look for, and how to structure a deal that maximises the profitability of your next development.

*The financial conditions detailed in this post are purely indicative and vary depending on the financial institution, the developer's profile, the specific characteristics of the real estate project, and market conditions at the time of application. The information provided does not constitute a binding offer or a guarantee of obtaining financing.

Table of Contents

- What is a Developer Loan?

- Characteristics and How It Works

- Advantages of the Developer Loan

- Ideal Situations for Applying

- Current Financial Conditions

- Requirements for Obtaining a Developer Loan

- Strategies for Optimising the Conditions

- Frequently Asked Questions

What is a Developer Loan?

The developer loan is a specialist financial instrument designed specifically for the real estate and construction sector. It is a bank or private financing product structured to fund the costs of developing a real estate project across all its phases — from land acquisition through to construction completion.

What sets it apart from other financing products is its progressive drawdown structure, commonly referred to as "tranches", which is tied to construction certifications or specific build milestones reached during the project.

This structure means the developer receives capital as construction progresses — rather than all at once upfront — which optimises financing costs by ensuring interest is paid only on the capital actually drawn down, not on the full loan amount.

Characteristics and How It Works

The developer loan operates according to a well-defined framework:

1. Review and Approval

The financial institution carries out a thorough analysis of:

- Technical and economic viability of the project

- Location and characteristics of the site

- Detailed budget and construction schedule

- Sales and marketing forecast

- Experience and financial strength of the developer

2. Loan Formalisation

Once approved, the following are established:

- Maximum financeable amount (generally between 60–80% of total cost)

- Financial terms (interest rate, fees, repayment period)

- Drawdown schedule tied to construction certifications

- Required security (mortgage, personal guarantees, etc.)

3. Progressive Drawdowns

Capital is released in stages through:

- Periodic certifications of construction progress

- Technical verification by the institution

- Confirmation that build milestones have been reached

- Adherence to the pre-agreed drawdown schedule

4. Repayment

Repayment is typically structured through:

- Partial repayments linked to the sale of individual units

- A final maturity date for any remaining balance

- The option of early repayment (generally without penalty)

A defining feature of the developer loan is its temporary, project-specific nature. It is designed for the construction phase, with a time horizon that rarely exceeds 36 months — covering both the build period and a margin for marketing the completed units.

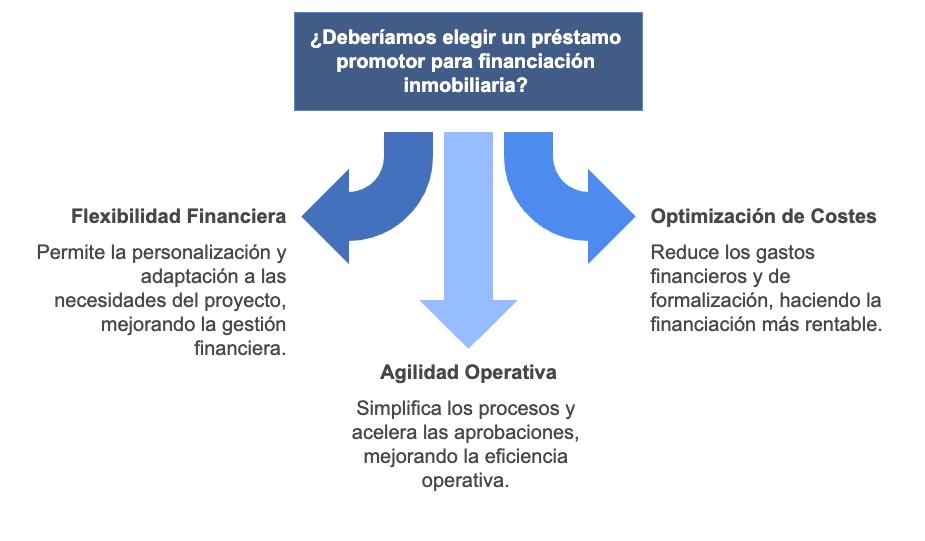

Advantages of the Developer Loan

The key advantages of the developer loan over other real estate financing alternatives are:

Flexibility and Adaptability

- Drawdowns matched to construction progress: Capital arrives in line with actual cash flow needs as the build advances.

- Tailored conditions: Greater scope for negotiation and adaptation to each project's specific circumstances.

- Modular structuring: Different tranches can be set up for different project phases — acquisition, construction, and marketing.

Financial Optimisation

- Repayments tied to sales: Financial obligations align with the revenue coming in from unit sales.

- Efficient use of capital: In many structures, interest is charged only on funds drawn down, not on the total facility.

- Lower upfront costs: Arrangement fees and set-up costs are generally lower than those of other mortgage instruments.

Operational Agility

- Simpler documentation: Fewer registration and notarial formalities than a full developer mortgage.

- Faster approval: Review and decision timescales are typically shorter.

- Greater flexibility for amendments: Easier to adjust conditions if the project changes or unforeseen issues arise.

Ideal Situations for Applying

The developer loan is particularly well suited in the following scenarios:

Developer Profiles

- Developers with a proven track record: Prior history is viewed positively by lenders and leads to more favourable terms.

- Developers running multiple projects simultaneously: Allows each transaction to remain financially independent.

- Developers with strong sales capabilities: Ideal for those with effective distribution channels who can move units quickly.

Project Types

- Developments with parallel marketing: Where sales activity begins during the construction phase.

- Developments with strong pre-sales: A high level of pre-sold units significantly improves the terms on offer.

- Phased developments: Where the scheme is delivered in stages, allowing financing to be calibrated to the actual pace of development.

- Developments in high-demand locations: Areas where rapid take-up is expected once construction completes.

Current Financial Conditions

The terms available on developer loans have evolved considerably in recent years. The Spanish market in 2025 has a number of distinctive characteristics every developer should be aware of:

Financial Cost Structure

- Variable components: Typically linked to Euribor, adjusting with market conditions and the project's risk profile

- Upfront costs: Include arrangement, underwriting, and loan origination fees

- Ongoing costs: Related to management, monitoring, and construction certification reviews

Financing and Guarantees

- Percentage of financing relative to total cost: Varies with the developer's profile and project characteristics

- Loan-to-value ratio (LTV): Calculated on the appraised value of the completed project, with limits set by each institution's risk policy. This ratio can reach up to 70% in some situations.

- Typical security:

- Mortgage over the land and future construction

- Personal guarantees from major shareholders

- Assignment of receivables from exchange contracts

Factors That Improve Conditions

- Level of pre-sales: A meaningful share of units exchanged before the first drawdown

- Prior experience: Developers with a verifiable history of completed projects receive more favourable terms

- Project sustainability: High energy ratings (A or B) are increasingly factored into lenders' assessments

- Strategic location: Projects in high-demand, low-supply areas attract stronger valuations

- Corporate solvency: The developer's financial structure and balance sheet strength directly influence the terms offered

- Architectural quality: Designs from recognised firms with a strong track record add value in the assessment process

Are you planning your next real estate development? Contact us today for a free initial assessment of your project. Our team will respond within 24 hours with an evaluation of the financing options tailored to your specific case.

Requirements for Obtaining a Developer Loan

The documentation and solvency requirements for a developer loan include:

Corporate Documentation

- Articles of incorporation and powers of attorney

- Annual accounts for the last 3 financial years

- Tax returns (corporate tax, VAT, personal income tax of shareholders)

- Credit register and up-to-date bank statements

- Real estate track record of the company and its principal shareholders

Project Documentation

- Title deed to the land

- Building permit or status of the planning application

- Approved outline or detailed design project

- Detailed budget and construction programme

- Market study and sales strategy

- Pre-contracts or signed reservations (where applicable)

Requirements for Developers Without Prior Experience

For first-time developers, lenders typically impose additional conditions:

- A substantially higher equity contribution (minimum 30–40% of total cost)

- Significant additional security beyond the project itself

- A technical team with a demonstrable track record (architects, project managers, main contractors)

- A higher level of pre-sales (typically >30% before the first drawdown)

- A comprehensive viability study, preferably prepared by an independent consultancy

Strategies for Optimising the Conditions

How you approach the process can make a significant difference to the terms you achieve:

Thorough Preparation

- Compile a professional, complete financing dossier

- Commission a rigorous market study

- Present realistic, well-supported financial projections

- Obtain independent technical certifications and valuations

Strategic Negotiation

- Request offers from multiple institutions at the same time

- Negotiate each cost component separately — rate, fees, and security requirements

- Link improved terms to sales milestones

- Propose tranche-based or mixed structures that reflect actual project progress

The Value of Specialist Advice

The financial impact of working with specialists can be substantial. Transactions intermediated by experts such as GrupInversor can achieve financing costs that are 5–20% lower overall.

Specialist advice is especially valuable for:

- Developers with limited experience

- Projects with unusual or complex characteristics

- Transactions involving sophisticated financial structures

- Deals of significant scale

At GrupInversor we have over 20 years of experience advising real estate developers on optimising their financing structure. Our specialist team analyses each project individually and negotiates with multiple institutions to secure the best possible terms for your developer loan.

Do you have a real estate project in mind? Are you looking for a developer loan? Contact us for a personalised assessment and to discover the optimal financing option for your next development.

Frequently Asked Questions

What are the main differences between a developer loan and a developer mortgage?

The developer loan offers greater flexibility, lower upfront costs, and shorter terms (12–36 months), making it primarily suited to the construction phase. A developer mortgage provides a higher percentage of financing and allows individual mortgages to be subrogated to end buyers, but involves higher arrangement costs and greater documentary complexity.

What happens if I cannot sell all the units within the developer loan term?

In that situation, several options are available:

- Negotiate an extension of the maturity date (usually with revised conditions)

- Refinance through individual mortgages over the unsold units

- Arrange alternative financing to repay the original loan

Is it possible to obtain a developer loan for comprehensive refurbishment projects, or does it only apply to new construction?

Yes, developer loans are perfectly viable for comprehensive refurbishment — they are not limited to new build. In fact, roughly 20% of developer loans granted in Spain relate to significant refurbishments, particularly in historic city centres and established tourist areas. To qualify under this instrument, the works generally need to affect structural elements or generate a significant uplift in value (>40–50%). Lenders tend to view positively refurbishment projects in prime locations where new development is constrained. The factors most closely assessed include the technical quality of the refurbishment design, compliance with current regulations (especially energy efficiency standards), and the marketability of the finished product.

What is the minimum equity contribution typically required?

The required equity contribution varies with the developer's profile and project characteristics, but generally falls between 20–40% of total cost for developers with a verifiable track record. The value of land already owned by the developer can be counted towards this contribution.

What minimum requirements must I meet to apply for a developer loan without prior experience?

For first-time developers, lenders typically require: a significantly higher equity contribution (minimum 40–50% of total cost); substantial additional security beyond the project itself; a technical team with a proven track record (architects, project managers, and main contractors); a higher level of pre-sales (typically >40% before the first drawdown); and a detailed viability study prepared by a recognised independent consultancy. It is also strongly advisable to engage a specialist to help prepare the financing dossier, which substantially improves the chances of approval.

What are the current conditions for a developer loan in Spain and how do they compare with previous years?

Conditions for developer loans in Spain have stabilised in recent years. In 2025, maximum LTV ratios generally sit between 60–70% of appraised value. This represents an improvement over the 2018–2020 period, when average LTVs rarely exceeded 60%. That said, documentary and solvency requirements have become more stringent, with greater emphasis on project quality and the developer's financial sustainability. Energy efficiency and sustainability credentials are increasingly weighted in lenders' assessments and can improve terms for projects with high energy ratings.