How to Mitigate Risk in Property Flipping Operations

Introduction: Risk Management in Property Flipping

Despite its attractive returns, property flipping carries significant risks that can seriously jeopardise the financial success of a project. As a companion to our recent guide on the 7 strategic renovations that maximise ROI in property flipping, this article takes a closer look at the main risks associated with this investment strategy and offers practical solutions for managing them effectively.

The fundamental difference between investors who achieve consistent success and those who fail in their flipping projects comes down primarily to their ability to anticipate, quantify, and manage these risks in a systematic, professional way. At GrupInversor, after two decades helping to structure financing for real estate developers and property flipping projects, we have identified the critical factors that can threaten profitability — and the most effective strategies for protecting your investment.

IMPORTANT DISCLAIMER: The content of this article is for informational purposes only. The information provided does not constitute financial, legal, tax, or investment advice. The strategies, data, and figures on returns mentioned are estimates based on general market conditions and may vary significantly depending on the particular circumstances of each investor, property, location, and economic environment. The author and publisher of this content accept no liability for decisions readers may make based on this information.

Table of Contents

- Introduction: Risk Management in Property Flipping

- Key Points for Mitigating Property Flipping Risks

- Main Risks in Flipping Projects

- Mitigation Strategies and Contingency Plans

- The Financial Factor in Risk Management

- Conclusion: Risk Management as a Competitive Advantage

- Next Steps

- Frequently Asked Questions

Key Points for Mitigating Property Flipping Risks

- Approximately 72% of flipping projects experience cost overruns of at least 15% above the initial budget.

- Each month of unplanned delay reduces profitability by roughly 1–1.5% in annualised terms.

- Financial safety reserves should cover 15–25% of the total renovation budget to absorb unforeseen costs.

- Specialist insurance for property flipping projects costs only 0.5–1.5% of the total budget and provides critical protection.

- Diversifying your financing sources significantly reduces project vulnerability.

- Grace periods in financing must cover the estimated project duration plus a buffer of at least 30%.

- Professional, systematic risk management can become a decisive competitive advantage over other investors.

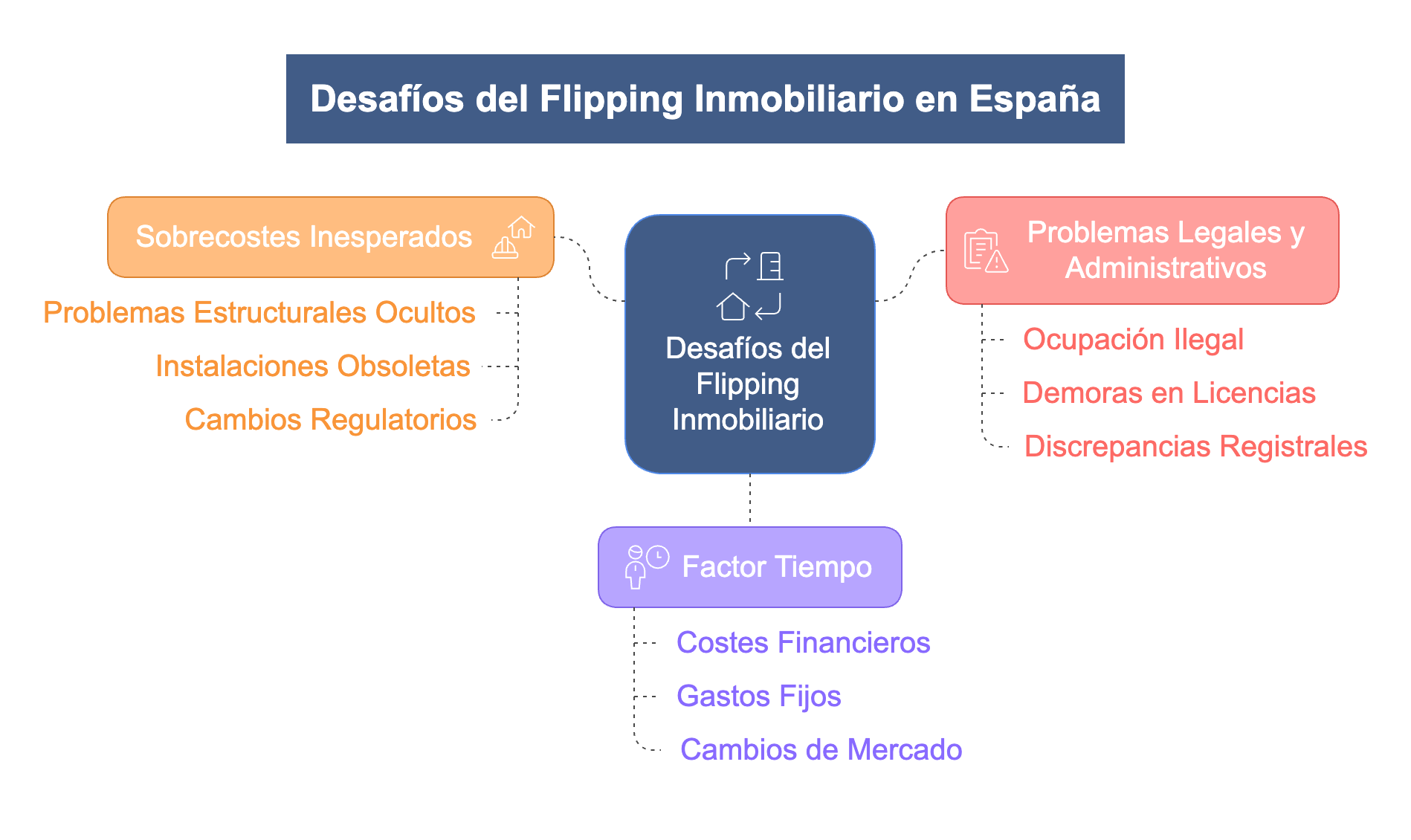

Main Risks in Flipping Projects

1. Unexpected Cost Overruns During Renovations

Industry statistics show that roughly 72% of property renovation projects in Spain exceed their initial budget by at least 15%. This is one of the main reasons flipping projects fail to deliver the expected returns.

Main causes of cost overruns:

Four recurring factors consistently drive significant budget deviations:

-

Hidden structural problems: Dampness not initially detected, aluminosis, foundation deficiencies, or settlement issues that only come to light once renovation work begins. These can push the budget up by 20–40%.

-

Obsolete or non-compliant installations: The need to fully replace electrical systems, plumbing, or HVAC that were initially expected to be partially retained. Complete replacement can account for up to 25% of the total budget.

-

Regulatory changes or additional requirements: Unexpected demands from local authorities, residents' associations, or utility companies that require modifying the original scope or adding elements not in the original plan.

-

Errors or omissions in initial planning: Items left out of the budget, underestimated unit costs, or miscalculated quantities of materials and labour.

How to mitigate unexpected cost overruns in your flipping projects:

Preventing overruns requires a multidisciplinary approach that combines:

- Thorough pre-purchase technical inspections by qualified specialists, covering structural analysis, installation reviews, and detection of hidden defects.

- Budgets that include specific contingency allowances of 15–20% above the estimated cost for each section of work.

- Detailed contracts with suppliers and contractors that set out precise specifications and penalties for non-compliance or delays.

- A full legal due diligence process to identify any regulatory restrictions or special requirements applicable to the property.

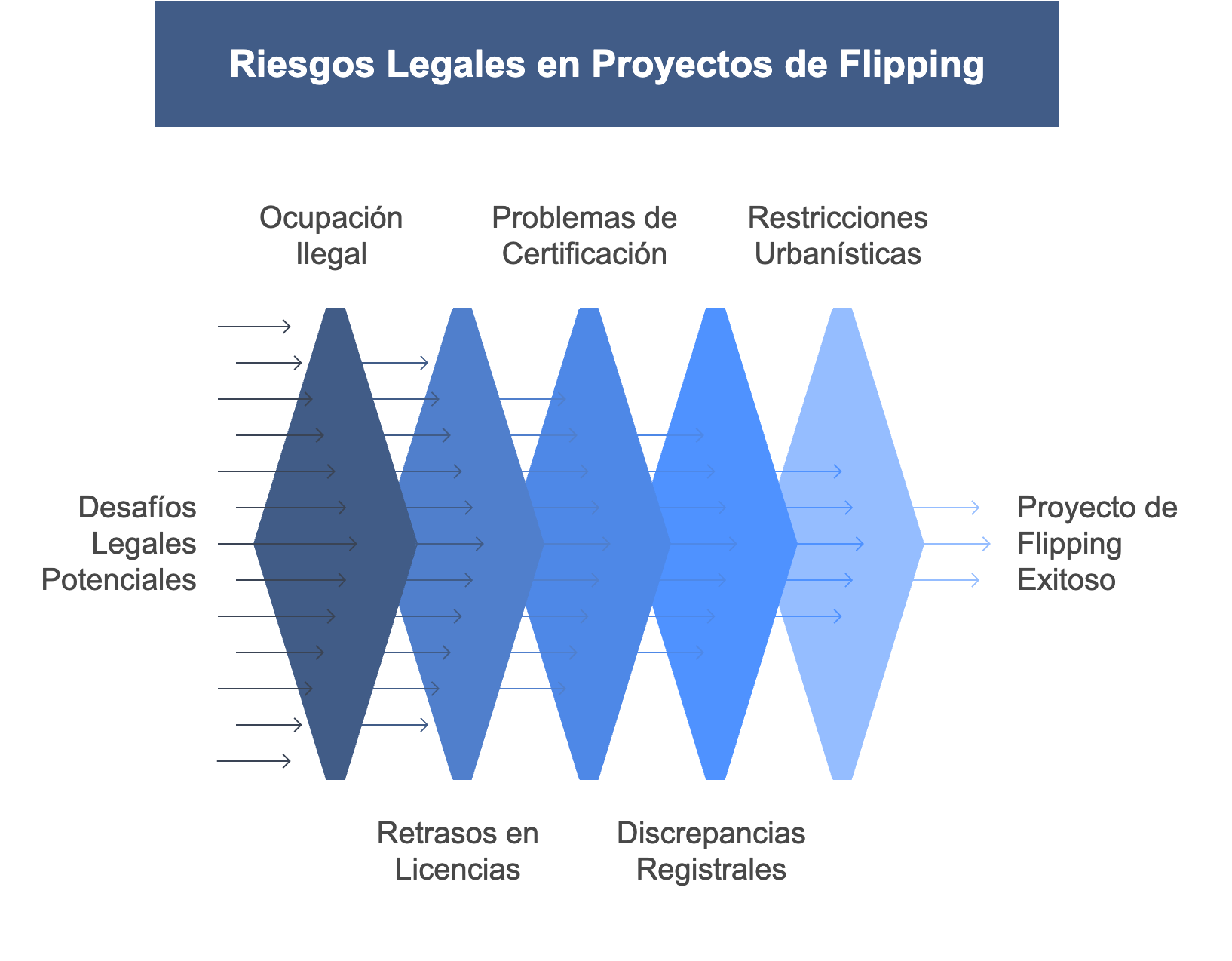

2. Legal and Administrative Problems

Legal and administrative obstacles can stall a flipping project for months or make it completely unviable, directly eroding your return on investment.

Most common legal risks:

Analysis of problematic cases reveals five recurring situations that cause significant complications:

-

Illegal occupation of the property: Can cause major delays in accessing the property, with eviction proceedings that drag on for months and substantially increase financial holding costs.

-

Delays in obtaining permits: Timescales for municipal permits can stretch considerably, especially for comprehensive renovations or those affecting structural elements. In some areas, delays can exceed 6–8 months.

-

Problems with mandatory certifications: Difficulties obtaining habitation certificates, energy performance certificates, or technical building inspections, particularly in older properties or those with unregistered modifications.

-

Land Registry discrepancies: Differences between the physical reality of the property and its registered description, which can complicate both financing and the eventual sale.

-

Unforeseen planning restrictions: Specific restrictions on listed buildings, particular local regulations, or undocumented easements that limit what can be done in the renovation.

Preventive measures to avoid legal and administrative risks:

Getting ahead of these risks is essential. To protect your flipping projects, carry out:

- Prior consultation with specialists in planning law and local regulations who know the specific area.

- A thorough check of actual occupancy status through in-person visits and enquiries with neighbours and property managers.

- A detailed review of the specific regulations applicable to the property and its surroundings.

- Research into typical permit timescales in the area where the property is located.

- A review of the residents' association bylaws and any restrictions that could affect the project.

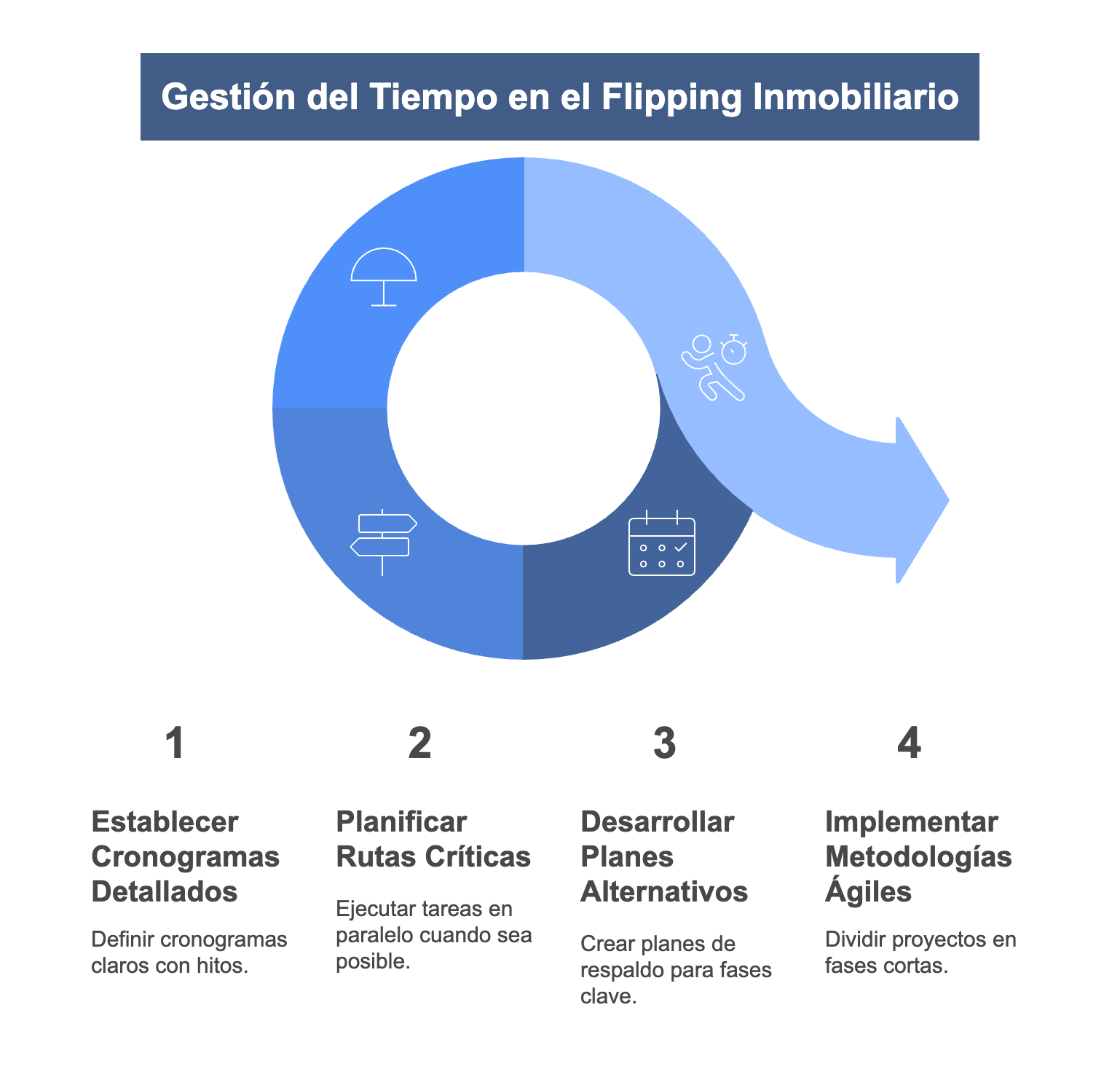

3. The Time Factor as a Risk Multiplier

In property flipping, time is not just a scarce resource — it is a genuine risk multiplier that directly affects project profitability. Each additional unplanned month simultaneously increases:

- Financial costs from loans and credit lines.

- Fixed expenses tied to property maintenance.

- Exposure to adverse shifts in the property market.

- The opportunity cost of capital that remains tied up.

Key insight:

Analysis shows that for each unplanned month of delay, project profitability falls by roughly 1–1.5% in annualised terms. A flipping project targeting a 15% return that runs four months over schedule could see its effective profit drop to 9–11%.

Effective strategies for managing time and deadlines:

Sound time management requires a proactive approach that includes:

- Detailed schedules with clearly defined milestones and contractual penalties for delays.

- Critical path planning that allows activities to run in parallel wherever technically feasible.

- Contingency plans (Plan B) for each critical phase, so the project keeps moving even when unforeseen issues arise.

- "Agile renovation" methodologies that break the project into short phases with weekly reviews to catch and resolve any deviation quickly.

Mitigation Strategies and Contingency Plans

1. Financial Safety Reserves: How Much and How to Calculate Them

Adequate liquidity can determine whether a project survives an unexpected setback. Experience in the sector shows that financial reserves need to account for several different scenarios and needs.

Types of reserves required:

A solid reserve structure for property flipping projects should include:

-

A dedicated reserve for renovation overruns: Should represent 15–25% of the total renovation budget, varying with the age of the property and the complexity of the planned work.

-

A reserve for extended holding costs: Designed to cover a longer-than-expected sales period, including utilities, service charges, security, and maintenance.

-

A reserve for additional financing costs: Intended to cover possible extensions to loan or credit line terms, avoiding financial pressure that could force a hasty sale.

Practical method — The 3-2-1 Rule for financial reserves:

This quick calculation method sets three levels of protection:

- 3% of the total budget as the minimum reserve for straightforward projects in recently built properties

- 2 additional months of financing costs fully covered, including interest and fees

- 1 independent expert verifying all cost and timeline estimates

Are you planning your next real estate development? Contact us today for a free initial assessment of your project. Our team will respond within 24 hours with an evaluation of the financing options tailored to your specific case.

2. Specialist Insurance for Property Flipping Projects

The insurance market now offers products specifically designed for the risks of property flipping. These policies — costing 0.5–1.5% of the total project budget — provide critical protection:

-

All-risks construction insurance: Covers material damage during renovation works, including incidents caused by weather events, theft, or vandalism.

-

Specialist public liability insurance: Protects against third-party claims for damage caused during renovation, whether to people or to neighbouring properties.

-

Title insurance: Covers legal problems not detected during the purchase process, such as hidden encumbrances or title defects.

-

Bespoke flipping policies: Specifically designed to cover common contingencies in renovation projects, such as administrative delays, contractor disputes, or post-sale defects.

These policies not only provide direct financial protection but also improve financing terms by reducing the project's risk profile in the eyes of lenders.

The Financial Factor in Risk Management

A well-designed financial structure not only optimises the potential profitability of a flipping project — it is itself a powerful risk management tool.

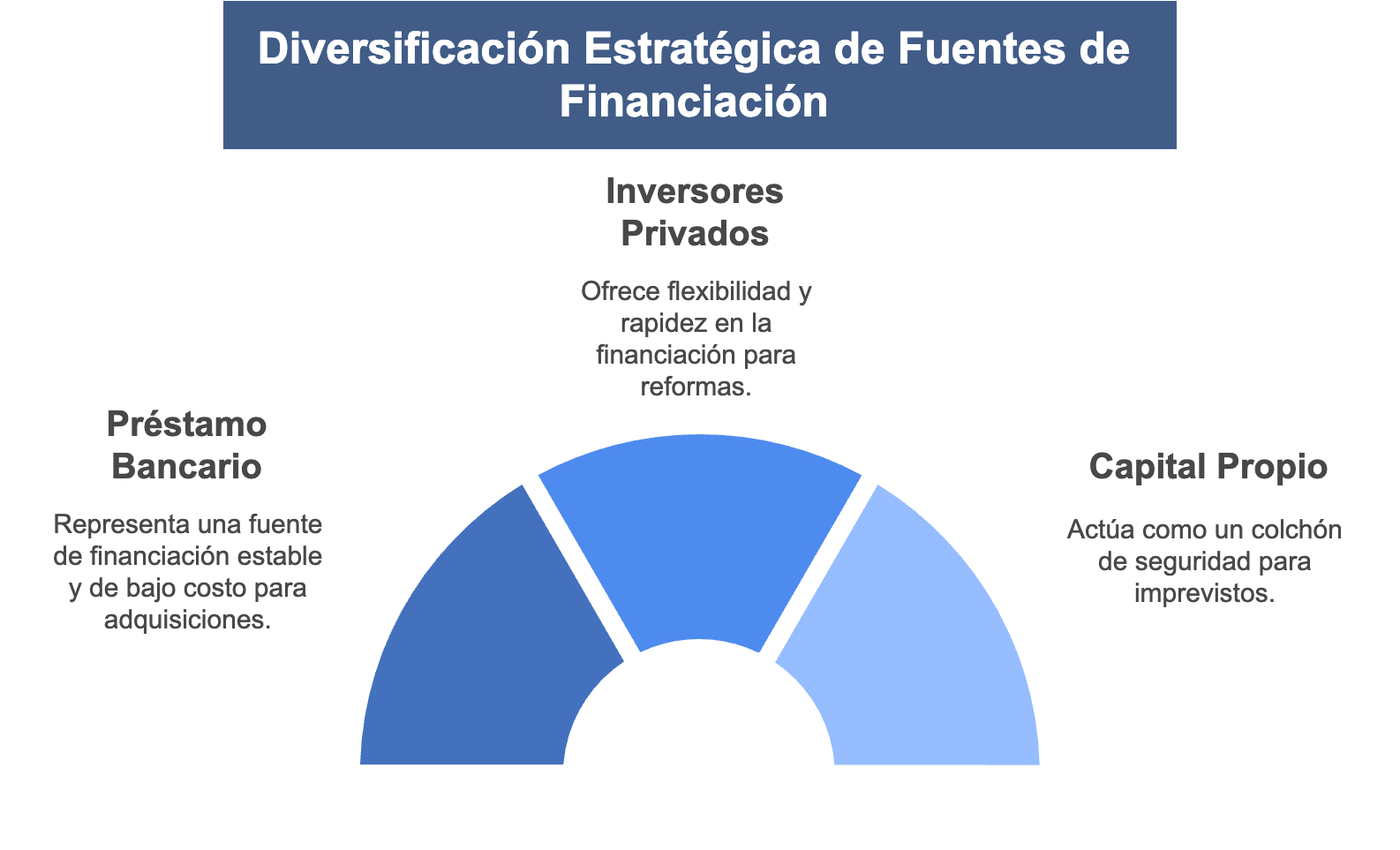

3. Strategic Diversification of Financing Sources

Over-reliance on a single financing source significantly increases a project's vulnerability to changing market conditions or issues specific to the lender.

Optimal financing structure:

Strategically combining different financial instruments can prove decisive. The most commonly used sources include:

- Traditional bank loan: Used primarily for property acquisition, benefiting from lower financial costs and more stable terms

- Private investor financing: Particularly suited to covering renovation costs, offering greater flexibility and faster access to funds

- Equity: Acts as a buffer against unforeseen costs and as collateral for other lenders

This diversification not only optimises the weighted average cost of capital but also significantly reduces exposure to the risks that come with dependence on a single lender.

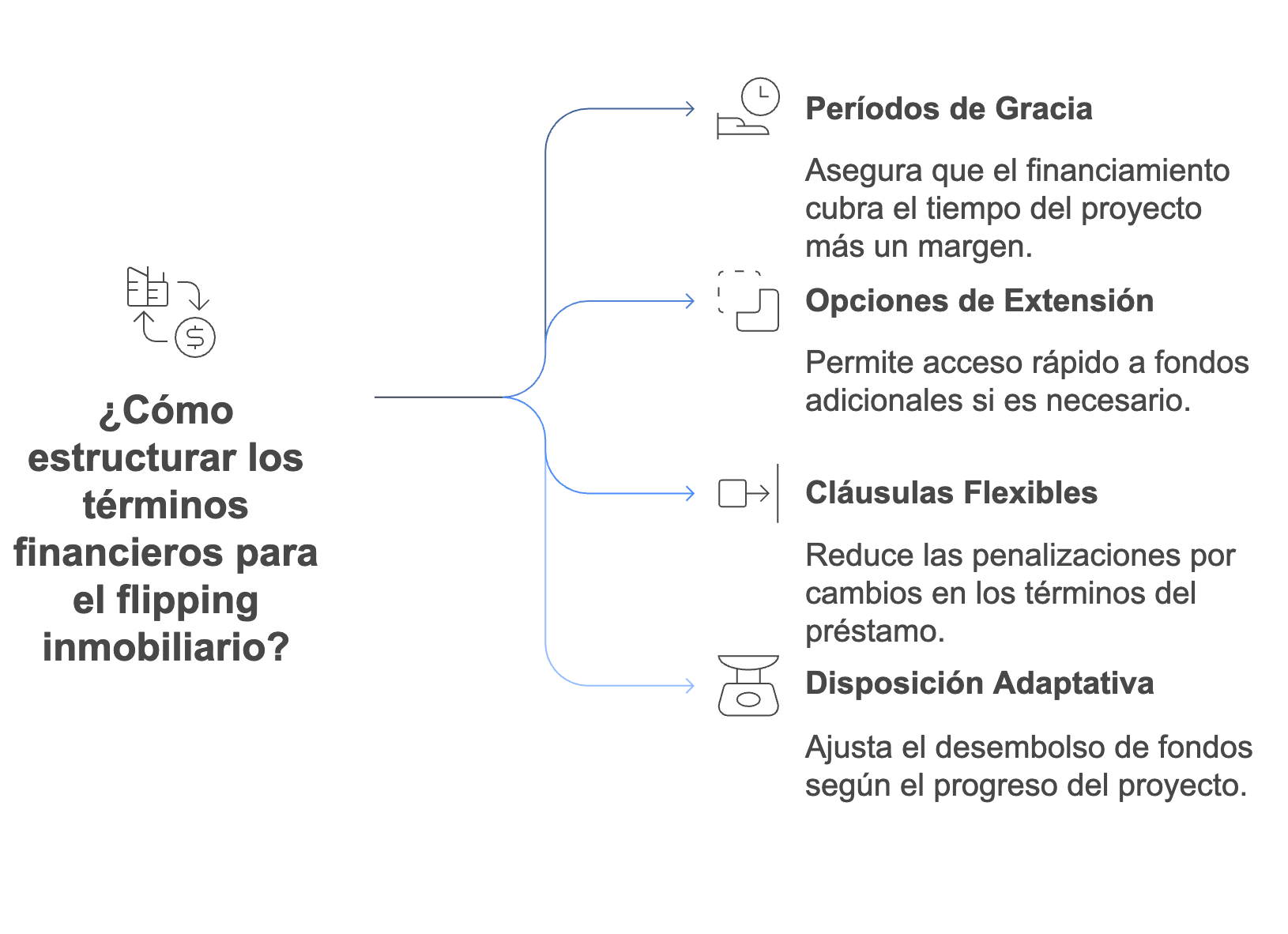

4. Financing Terms That Account for the Unexpected

When negotiating any type of financing for property flipping projects, it is essential to build in conditions that allow for deviations from the original plan:

- Generous grace periods: Must cover at minimum the estimated project duration plus a meaningful additional buffer.

- Pre-approved extension options: Pre-arranged supplementary credit lines that can be activated quickly if a contingency arises.

- Flexibility clauses: No significant penalties for early repayment or adjustments to conditions.

- Adaptive drawdown mechanisms: Systems that allow the pace of fund drawdowns to be matched to actual construction progress, keeping financial costs in check.

Structuring these elements carefully — as part of a developer loan specifically tailored for flipping — can mean the difference between riding out the inevitable complications and facing a financial crisis that puts the entire project at risk.

Conclusion: Risk Management as a Competitive Advantage

Professional, systematic risk management in property flipping has become a genuine competitive advantage that clearly separates occasional investors from consistently successful professionals. The right approach does not aim to eliminate all uncertainty — that is impossible in this sector — but rather to understand, quantify, and manage it in a way that the potential return justifiably compensates for the risk taken on.

As we explored in our guide on the strategic renovations that maximise ROI in property flipping, choosing the right improvements is fundamental to success — but it must be complemented by comprehensive risk management to ensure that projected returns are actually realised.

Investors who systematically build in risk analysis, appropriate reserves, specialist insurance, and resilient financial structures not only reduce the probability of failure — they also expand their ability to pursue opportunities that others would consider too risky.

Next Steps

If you are considering starting or improving a property flipping project, we recommend the following steps:

- Carry out a thorough, documented analysis of the specific risks associated with the property and its location

- Develop a detailed contingency plan with financial reserves sized to the complexity of the project

- Design a diversified financing structure that explicitly accounts for possible time and budget overruns

- Consult specialists on every critical aspect of the project — legal, technical, and commercial — before committing significant resources

At GrupInversor we have over two decades of experience helping investors secure the right financing for property flipping, construction, renovations, and all types of real estate developments, with tailored solutions that maximise the chances of success. If you think we can help, do not hesitate to get in touch.

Are you planning your next real estate development? Contact us today for a free initial assessment of your project. Our team will respond within 24 hours with an evaluation of the financing options tailored to your specific case.

Frequently Asked Questions

What are the most common risks faced by property flipping investors?

Investors in the Spanish market tend to underestimate three core risks:

- Renovation cost overruns (which typically run 15–30% above the initial budget),

- Execution timescales (which routinely extend 25–40% beyond what was planned), and

- The true costs of marketing (both financial and in terms of time).

To manage these risks effectively, we recommend working with an experienced specialist, building in wide safety margins for both budget and timeline, and conducting a thorough market study that covers a range of sales scenarios.

How does the specific location of the property affect the risks of a flipping project?

Location has a decisive influence on the overall risk profile. Properties in established, high-demand areas generally carry lower sales risk but come with tighter margins and stiffer competition. Emerging or transitional areas can offer higher margins but significantly increase the risks around sales timescales and valuation variability.

The best balance is usually found in well-established neighbourhoods that show clear signs of near-term appreciation — such as planned infrastructure improvements, positive demographic shifts, or urban regeneration projects in their early stages.

What percentage of the total budget should be set aside for contingencies?

Based on data from the Spanish real estate sector, successfully completed flipping projects typically allocate 15–25% of the total renovation budget for contingencies. This figure should be adjusted according to three key factors:

- The age of the property (older properties warrant a higher reserve percentage)

- The experience of the management team (first-time investors should increase the percentage significantly)

- The technical complexity of the planned renovation (projects involving spatial reconfiguration or structural work require larger reserves than purely cosmetic refurbishments)

Is it worth taking out specialist insurance for property flipping projects?

Absolutely. Insurance specifically designed for property flipping is a worthwhile investment, costing between 0.5–1.5% of the total project budget. The return on that cost comes not only from direct coverage of claims and contingencies — any one of which could threaten the viability of the entire project — but also from the peace of mind it brings to strategic decision-making and the better financing terms that many lenders offer to adequately insured projects.