Specialized Financing for Real Estate Developers: Beyond the Traditional Developer Loan

Introduction

The real estate developer loan is one of the most important financial tools for getting development projects off the ground. In a market where purpose-built construction finance is essential, this product offers solutions tailored to the specific needs of developers. At its core, a real estate developer loan is a specialist form of credit designed to finance construction and development projects — with characteristics that set it clearly apart from conventional financial instruments.

This guide covers everything you need to know about financing options, requirements, and alternatives for real estate projects, helping you make informed decisions that maximise the success of your developments.

Getting the financing structure right can be the difference between a project that delivers and one that struggles — particularly in a competitive market where capital efficiency is a decisive factor.

IMPORTANT NOTICE: The content of this article is for informational purposes only. The information provided does not constitute financial, legal, tax, or investment advice. The strategies, data, and return figures mentioned are estimates based on general market conditions and may vary significantly depending on the particular circumstances of each investor, property, location, and economic environment. The author and editor of this content accept no responsibility for decisions readers may make based on this information.

Table of Contents

- Introduction

- What is a Real Estate Developer Loan?

- Financing for Real Estate Projects

- Developer Loan Requirements

- How to Obtain a Developer Loan

- Financing for Residential Construction and Property Flipping

- Comparison and Financing Alternatives

- Conclusion

- Frequently Asked Questions

Key points about real estate developer loans:

- Developer loans provide specialist financing across the full real estate development cycle

- Funds are released in stages, tied to construction progress

- Lenders require financial soundness, prior experience, and a solid business plan

- Investment funds, crowdfunding, and joint ventures can complement traditional financing

- A strategic mix of financing sources typically delivers the best return on a project

What is a Real Estate Developer Loan?

A real estate developer loan is a dedicated credit product built to finance construction and real estate development projects. Unlike a standard mortgage — which is used to purchase a completed property — this instrument is designed to accompany a project through its entire development cycle.

Main Characteristics:

- Phased drawdowns: Funding is released in tranches aligned with construction milestones, verified by technical sign-offs at each stage.

- Flexible structure: Adapted to each phase of the development, from plot purchase through to practical completion.

- Technical monitoring: Includes professional oversight to ensure funds are deployed according to the agreed plan.

This phased mechanism benefits both developer and lender: it provides effective control over capital use while ensuring the project has the funding it needs at every stage.

At GrupInversor we work directly with financial institutions and specialist credit providers in this space. You can view some of our success stories on our main page about the developer loan.

If you are planning your next development and looking for financing, contact us. We will walk you through the options available.

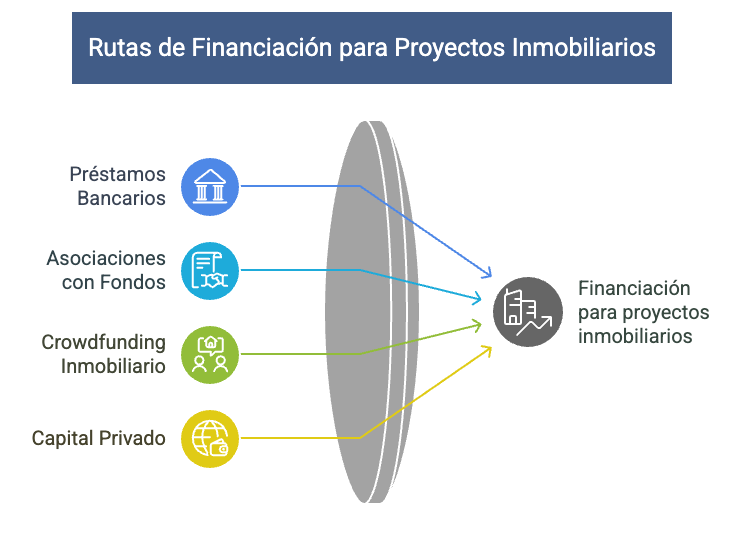

Financing for Real Estate Projects

The real estate project financing landscape is broad, with multiple options that complement the traditional developer loan. This range of choice allows developers to build a financial structure that genuinely fits the characteristics of each project.

Available Financing Options:

- Traditional bank loans: Offered by conventional financial institutions, with rigorous approval processes but potentially more competitive rates.

- Investment fund partnerships: Provide access to significant capital, especially useful for large-scale or innovative projects.

- Real estate crowdfunding: A modern approach that democratises access to financing through contributions from multiple investors.

- Private capital: Individual investors or family offices seeking real estate returns.

Each option has its own advantages and drawbacks, which need to be weighed against factors such as project scale, location, market segment, and the developer's track record.

Combining different financing sources strategically can optimise the project's overall capital structure — maximising profitability while keeping risk at a manageable level.

Developer Loan Requirements

Accessing a real estate developer loan means satisfying a set of specific requirements that lenders assess carefully to manage risk and confirm project viability.

Core Requirements:

-

Land ownership: In most cases, the land must be fully or partially paid for, demonstrating an upfront commitment from the developer.

-

Project viability: Lenders will expect to see:

- Detailed market studies

- Profitability analysis with financial projections

- A business plan consistent with the local market

-

Pre-sales or reservations: Many lenders require a minimum percentage of units sold or reserved before approving the loan — typically between 20% and 40%, depending on the market.

-

Technical and legal documentation:

- Construction licences and planning permissions

- Technical project signed off by the relevant professional body

- Developer's financial statements

- Clean credit history

- Demonstrable track record in comparable projects

Meeting these requirements not only improves the odds of loan approval — it can also positively influence the terms on offer, including interest rates and the percentage of costs financed.

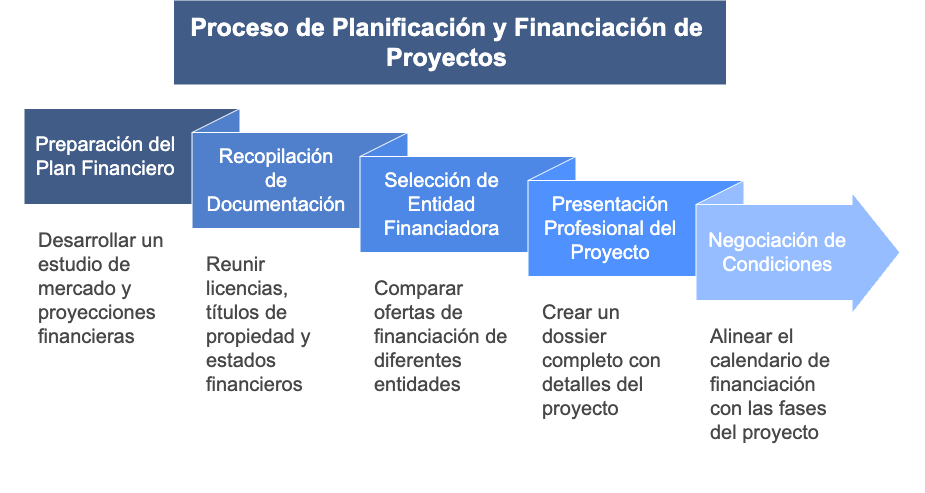

How to Obtain a Developer Loan

Securing financing for your real estate project requires a clear strategy and disciplined preparation. The following steps will significantly improve your chances of obtaining a developer loan.

Step-by-Step Process:

-

Prepare the financial plan

- Commission a thorough market study demonstrating genuine demand

- Build realistic financial projections with sensitivity analysis

- Identify and quantify key risks, with mitigation strategies for each

-

Gather the documentation

- Construction licences and planning permits

- Land title deeds

- Audited financial statements for the development company

- Track record of previous projects and details of the technical team

-

Select your lender

- Compare offers from traditional banks, investment funds, and alternative platforms

- Look beyond interest rates — assess terms, fees, and flexibility as well

-

Present the project professionally

- Assemble a complete pack with renders, plans, and technical specifications

- Highlight what makes the project distinctive and commercially compelling

- Include a detailed sales and marketing plan

-

Negotiate the terms

- Agree a drawdown schedule aligned with construction phases

- Push for amortisation clauses linked to sales proceeds

- Define clearly the milestones that will unlock each funding tranche

For more on current market conditions and strategies to optimise your financing terms, see our post on the developer loan: whether it is the right option for your real estate project.

Strategic Tips:

- Equity contribution: Having at least 30–40% of the total cost covered by your own funds significantly strengthens your negotiating position.

- Specialist advice: Working with a financial adviser who knows the real estate sector can make a real difference to how the deal is structured.

- Lender relationships: Building connections with financing institutions before you need them smooths the approval process and often improves the terms available.

These approaches not only help secure the financing — they also optimise the project's overall capital structure, directly improving the developer's margin.

Looking for financing for your real estate project? Contact us with no obligation. Our team will respond within 24 hours to assess the options available for your situation.

Financing for Residential Construction and Property Flipping

Residential construction financing has specific features that set it apart from broader developer lending. It is one of the most active and in-demand segments of the real estate market, and worth understanding in its own right.

Particularities of Residential Financing:

- More predictable sales cycles: Residential projects tend to follow more stable commercialisation patterns than commercial schemes, which simplifies financial planning.

- Greater risk diversification: Selling to multiple end buyers reduces dependence on any single purchaser.

- Subrogation potential: Residential loans can often be transferred to end buyers upon completion, which supports amortisation.

Specific Financing for Property Flipping

Property flipping requires a financing structure adapted to its short-cycle nature. Unlike traditional development, flipping projects need:

- Shorter terms: Typically 6–12 months, matched to the buy-renovate-sell cycle.

- Flexible drawdowns: Particularly around renovation milestones, where most of the added value is created.

- Bullet repayment structures: Designed to be repaid in full following the sale of the renovated property.

For a deeper look at this model and its financial dynamics, see our article on property flipping: a complete guide to investing and generating returns.

Key Aspects to Consider:

- Residential projects in prime locations or with sustainability credentials tend to access better financing terms.

- A strong track record in comparable residential schemes is viewed very positively by lenders.

- Adapting to current housing trends — flexible layouts, communal spaces, energy efficiency — has a measurable impact on project viability and financing options.

Getting the financing structure right for a residential development does not just determine whether it gets built. It directly affects the developer's profit margin.

Comparison and Financing Alternatives

The real estate developer loan is one option among many. Understanding the full range of alternatives is essential for selecting the financial structure that best fits each project's specific characteristics.

Comparative Table of Financing Options:

| Financing Option | Advantages | Disadvantages | Best Suited To |

|---|---|---|---|

| Bank Developer Loan | Competitive rates, high loan amounts | Strict requirements, slow approval | Developers with a track record and conventional projects |

| Alternative Financing | Greater flexibility, fast processes | Higher costs | Innovative projects or newer developers |

| Investment Funds | Large-scale capacity, added expertise | Partial cession of control | Major developments or prime locations |

| Real Estate Crowdfunding | Accessible, market validation | Capital limits, regulatory requirements | Small or mid-size projects with strong commercial appeal |

| Joint Ventures | Shared risk and resources | Management complexity | Strategic projects requiring specific expertise |

Determining Factors for the Choice:

- Project cash flow profile: Some instruments suit projects with early revenues; others tolerate a longer run before returns materialise.

- Developer track record: Traditional lenders place significant weight on prior experience, while alternatives can be more accessible for newer market participants.

- Location and asset type: Projects in prime locations or with well-established uses find it easier to access conventional financing.

- Flexibility requirements: If the project is likely to evolve during development, some instruments offer considerably more adaptability than others.

Looking for financing for your real estate project — whether to acquire land, renovate, or build from scratch? Contact us for a personalised assessment and to identify the right financing option.

Conclusion

The real estate developer loan remains a foundational financial tool for delivering successful developments in today's competitive market. This guide has examined its defining features, core requirements, and the process for obtaining one — providing a comprehensive view of this key real estate project financing instrument.

The right financing structure can determine whether a project succeeds or fails. The developer loan, with its phased drawdown approach tailored to the construction cycle, offers real advantages over other options — particularly for clearly staged projects delivered by developers with a solid track record.

That said, the real estate finance landscape continues to evolve, with new instruments emerging that complement traditional funding. A strategic combination of financing sources, matched to the specific characteristics of each project, typically delivers the optimal outcome: maximising profitability while maintaining control.

We recommend working with specialist real estate finance advisers before finalising the capital structure for your next project. Their knowledge of current market conditions can add genuine value to the planning process.

Planning your next real estate development or looking for property flipping finance? Contact us today for a free initial assessment. Our team will respond within 24 hours with a review of the financing options available for your specific project.

Frequently Asked Questions

What guarantees are required for a developer loan?

The main security requirements typically include a mortgage over the project (covering both land and future construction), personal guarantees from the principal shareholders, and in some cases additional collateral such as pledged equity or rights over future sales proceeds. The level of security required depends on the developer's profile and the nature of the project.

How long does the approval process take?

A traditional developer loan typically takes 2–4 months to approve, depending on project complexity and the lending institution. Private financing alternatives can cut this to 3–6 weeks, though generally on less favourable terms. Preparing all documentation thoroughly in advance — and presenting a strong business plan — can substantially accelerate the timeline.

Is it possible to combine different financing sources?

Yes — and for projects of any meaningful scale it has become standard practice. Blended or tranched financing allows the overall cost of capital to be optimised while maximising leverage. A typical approach uses bank lending for the senior layer, complemented by alternative financing for mezzanine tranches and equity for the remaining percentage. This structure needs to be carefully set up to avoid conflicts between the different providers.