Financing for Land and Plot Purchase

If you are planning a real estate development, acquiring the land or plot is the first critical step toward making it viable. Securing the right land purchase financing can mean the difference between seizing a profitable opportunity and watching it slip away.

Below, we explore the best options, strategies, and practical guidance for obtaining the financing you need to purchase the site on which to build your project.

IMPORTANT NOTICE: The content of this article is for informational purposes only. The information provided does not constitute financial, legal, tax, or investment advice. The strategies, data, and return figures mentioned are estimates based on general market conditions and may vary significantly depending on the particular circumstances of each investor, property, location, and economic environment. The author and editor of this content accept no responsibility for decisions readers may make based on this information.

Table of Contents

- Key Points for Buying Land and Acquiring Plots

- What is Financing for Land Purchase?

- Financing Options and Methods

- Financing for Developable Land

- Financing Strategies for Real Estate Developers

- Preparation Prior to Financing Application

- Process and Negotiation of Financial Conditions

- Common Mistakes to Avoid in Land Financing

- Conclusion

- Frequently Asked Questions

Key Points for Buying Land and Acquiring Plots

- Securing the right financing to acquire the land or plot for your development requires detailed analysis and thorough documentation.

- There are multiple alternatives beyond traditional banking, each suited to different project profiles.

- Whether the land is fully serviced or still developable has a significant impact on the financing terms available.

- Real estate developers can draw on specific strategies to optimise their financial structure.

- Thorough preparation substantially increases the likelihood of approval on favourable terms. For this reason, we always recommend seeking advice from independent experts.

What is Financing for Land Purchase?

Land purchase financing is a specialist segment within the broader real estate finance market. It differs from other lending products in several important ways, as it is designed specifically for the acquisition of land — whether for immediate development or as a longer-term investment.

Fundamental Characteristics

Loans for land acquisition typically share the following features:

- Shorter terms than conventional mortgages (generally between 2 and 10 years)

- Higher equity requirements (usually 25–50% of the land value)

- Interest rates above standard mortgage levels, reflecting the nature of land as collateral

- Greater emphasis on the quality and development potential of the land than on the borrower's credit profile alone

- A requirement to present clear and credible development plans

Financing is available across different land types, from fully serviced urban plots to undeveloped rural sites, each with its own valuation approach and lending requirements.

Types of Financing According to Land Classification

The appropriate financing structure depends on the development status and classification of the land:

-

Financing for developed (serviced) land: For plots that already have utilities and infrastructure in place. These loans typically carry more favourable terms due to their lower risk profile.

-

Financing for developable land: For land classified as suitable for residential or commercial development under current planning regulations, but not yet serviced. Lenders will require a credible urbanisation plan.

-

Loans for rural land: For land without urban classification, primarily intended for agricultural or recreational use. These generally come with more restrictive conditions.

Each loan application involves a thorough review of current land value, future potential, applicable planning restrictions, and the feasibility of the proposed project. If the plan is to develop the land rather than hold it, the natural next step is a developer loan that finances both the land and the construction in a single structure.

Looking for financing to purchase land and begin building? Contact us with no obligation. Our team will get back to you within 24 hours to assess the options available for your situation.

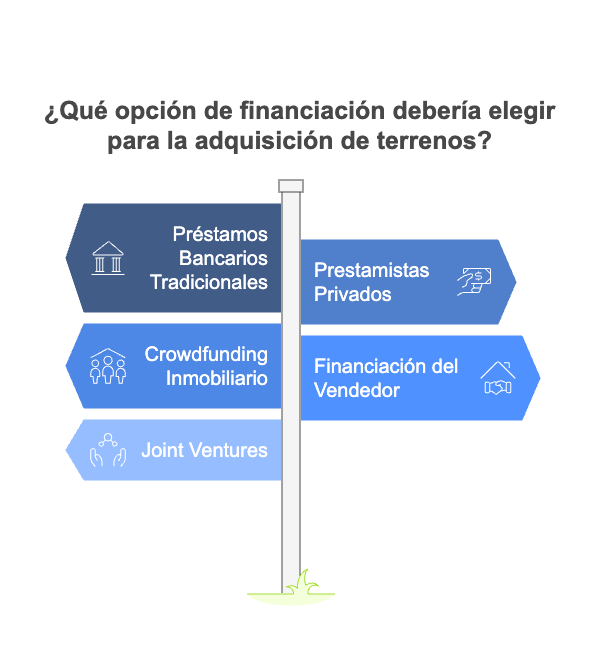

Financing Options and Methods

The market offers a range of approaches to land purchase financing, each with its own advantages, requirements, and trade-offs. Understanding them in depth will help you identify the most suitable route for your project.

Traditional Bank Loans

Commercial banks offer several products for land acquisition:

-

Mortgage loans for land: Structured similarly to a conventional mortgage, using the land as collateral. These typically require a substantial deposit (30–50%) and have terms of 5–15 years.

-

Real estate credit lines: Provide flexibility for multiple acquisitions under a single credit facility. Well suited to developers with several projects running in parallel.

-

Bridge loans: Short-term financing to cover the acquisition while permanent financing is arranged or the project is developed.

Bank lending in this area is generally characterised by rigorous approval processes, extensive documentation requirements, and detailed feasibility assessments.

Alternative Financing

Beyond traditional banking, a number of alternative routes exist:

-

Private lenders: Specialist investors or companies that offer financing with greater flexibility, though typically at higher rates. Approval tends to be faster.

-

Real estate crowdfunding: Platforms that raise capital from multiple individual investors. Well suited to projects with a compelling story or social angle.

-

Seller financing: Arrangements in which the landowner accepts deferred payments, reducing or eliminating the need for external bank finance.

-

Joint ventures: Partnerships with equity investors who contribute part of the required capital in exchange for a share of future profits.

These alternatives are particularly valuable when traditional channels are inaccessible, or when a more flexible, bespoke structure is needed.

Mixed Financing and Combined Strategies

For complex projects, combining different financing sources can optimise the overall capital structure:

- Using equity for the initial deposit and external financing for the balance.

- Pairing short-term acquisition loans with long-term refinancing once early development is complete.

- Structuring phased drawdowns aligned with the development timetable.

This approach can reduce the total cost of financing and spread risk across different instruments and time horizons.

Financing for Developable Land

Developable land has specific characteristics that directly shape the financing available for it. Its future development potential makes it an attractive category for investors and developers, though it also comes with particular considerations.

Characteristics of Developable Land

Developable land is typically defined by:

- A planning classification that permits development.

- The need for urbanisation works before construction can begin.

- Significant potential for value appreciation once developed.

- Specific planning rules governing permitted uses and buildability.

These characteristics directly influence how lenders assess and structure loans for its acquisition.

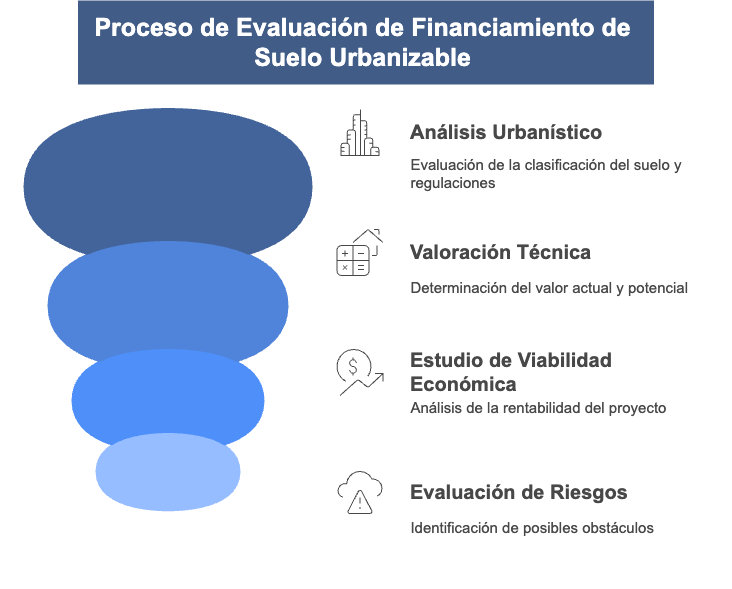

Valuation and Assessment Processes

Financing for developable land involves a more involved assessment process:

-

Planning analysis: A detailed review of the land's classification, permitted buildability, planning obligations, and expected development timelines.

-

Technical valuation: An assessment of current value and post-development potential, taking into account urbanisation costs and projected timescales.

-

Economic feasibility study: A full profitability analysis covering the entire project, from acquisition through to final sale.

-

Risk assessment: Identification of potential planning, technical, or market obstacles that could affect the development.

Lenders typically require comprehensive reports prepared by specialist professionals to support these assessments.

Optimal Structure for Financing Developable Land

Given the evolving nature of developable land, financing is usually structured to reflect the different phases of the development process:

- Initial financing for land acquisition

- Supplementary funding to cover urbanisation costs

- Refinancing or restructuring once urbanisation is complete

- Possible additional financing for the construction phase

This phased approach aligns financial commitments with the growth in asset value over time, reducing the overall risk of the project. Be sure to review the financing options available for developers.

Specific Requirements

To secure financing for developable land, lenders will generally expect:

- A meaningful equity contribution (typically 20–30% of the acquisition price)

- A detailed business plan with sensitivity analysis

- Demonstrable experience in comparable projects

- Additional security or collateral in many cases

- Realistic development and sales timelines

Meeting these requirements thoroughly will significantly improve your chances of obtaining financing on favourable terms.

Financing Strategies for Real Estate Developers

Land can account for 30–50% of a project's total cost, making the financing strategy for its acquisition a critical decision. The following proven approaches can maximise your chances of success.

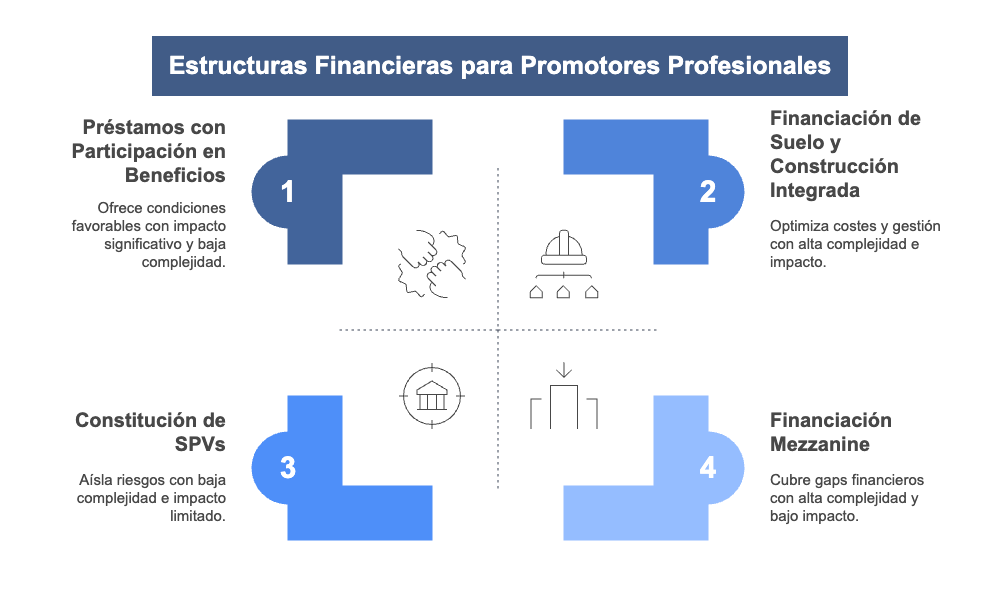

Advanced Financial Structures

Experienced developers have access to more sophisticated structures:

-

Integrated land and construction financing: Negotiating a single package covering everything from acquisition to practical completion, simplifying management and reducing overall cost.

-

Profit participation loans: Structures in which the lender accepts a lower interest rate in exchange for a share of the project's future profits.

-

Mezzanine financing: A hybrid instrument sitting between senior debt and equity, used to bridge the gap between the main loan and the required equity contribution.

-

SPV (Special Purpose Vehicle) structures: Creating a dedicated company for each project, isolating risk and optimising the financial and tax structure.

These structures require specialist advice but can deliver a meaningful competitive advantage.

Effective Negotiation with Financial Institutions

Strong negotiation skills can make a substantial difference to the terms you achieve:

-

Document your track record professionally: Present previous successful projects in detail, highlighting on-time delivery and budget discipline.

-

Compare lenders systematically: Research multiple institutions to identify the best terms and the most productive points for negotiation.

-

Present tailored structures proactively: Rather than waiting to respond to a standard offer, propose a financial structure that suits your project's risk profile and cash flow characteristics.

-

Negotiate for flexibility: Push for clauses that allow adaptation to unforeseen events, such as grace periods or penalty-free early repayment options.

Developers who approach lenders strategically — with the project clearly framed and the numbers well presented — consistently achieve better rates, longer terms, and lower security requirements.

Practical Cases and Step-by-Step Guide to Successfully Purchasing Your Land

Securing land purchase financing requires a methodical approach. The following step-by-step guide covers the key actions that give you the best chance of success.

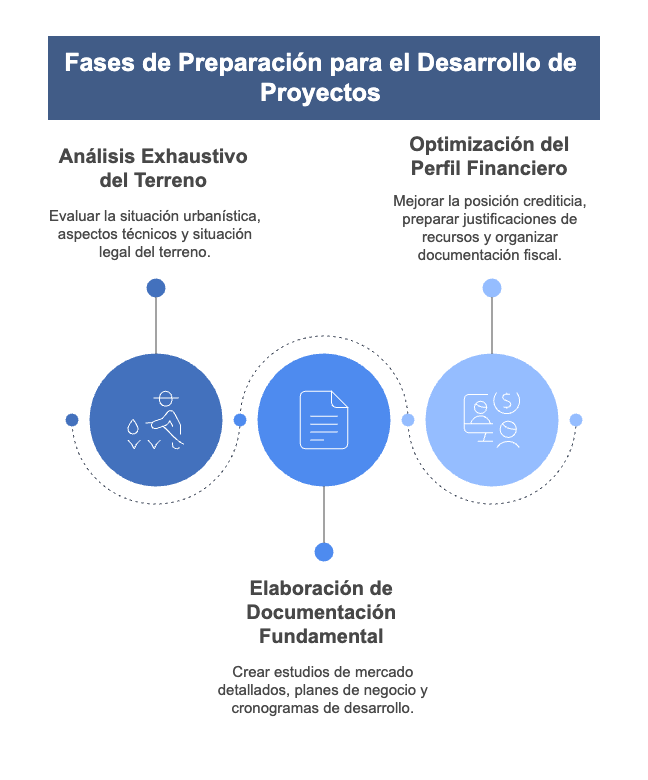

Preparation Prior to Financing Application

-

Thorough due diligence on the land

- Confirm the exact planning status (classification, permitted buildability, obligations).

- Review technical factors (topography, ground conditions, access, available services).

- Check legal title (clear ownership, encumbrances, easements).

- Assess any environmental or archaeological risks.

-

Preparation of core documentation

- A detailed market study based on current data.

- A business plan with realistic financial projections.

- A sensitivity analysis covering different scenarios.

- A detailed development and delivery programme.

- Evidence of experience in comparable projects.

-

Strengthening your financial profile

- Review and improve personal or corporate credit standing where possible.

- Prepare a clear account of available equity.

- Arrange additional security if required.

- Ensure tax and accounting records are well organised and transparent.

This preparation phase takes time and effort, but it is essential to success at every stage that follows.

Process and Negotiation of Financial Conditions

-

Strategic selection of lenders

- Identify institutions that specialise in real estate financing.

- Approach multiple lenders to compare terms.

- Consider both traditional and alternative sources.

- Factor in the experience of other developers with each institution.

-

Presenting the project effectively

- Tailor your documentation package to each lender.

- Prepare a professional and persuasive visual presentation.

- Highlight the project's differentiating factors and competitive strengths.

- Anticipate the questions and objections you are likely to face.

-

Negotiating the terms

- Compare offers on a like-for-like basis.

- Identify where each proposal can be improved.

- Negotiate beyond the headline rate — fees, terms, grace periods all matter.

- Seek flexibility to accommodate unexpected developments.

Presenting the project clearly and negotiating from an informed position can make a significant difference to the final terms.

Common Mistakes to Avoid in Land Financing

Keep these common pitfalls in mind as you prepare:

-

Underestimating timelines: Land financing takes longer than most people expect. Build realistic time buffers into your plan from the outset.

-

Incomplete documentation: Submitting thin or poorly prepared files creates doubt and delays. Invest the time to make your application thorough and clear.

-

Superficial market analysis: General impressions are no substitute for concrete, up-to-date data. Use reliable sources and rigorous analysis.

-

Overlooking key planning issues: Failing to identify restrictions or encumbrances that could affect the development. Carry out a full planning due diligence.

-

Overly optimistic projections: Presenting best-case scenarios undermines your credibility. Work with conservative, well-supported estimates.

Avoiding these mistakes can be the difference between approval and rejection.

Conclusion

Land purchase financing is a foundational element of successful real estate development. This guide has covered the full range of options available — from traditional bank loans through to more innovative and flexible alternatives — as well as the specific challenges of developable land and the advanced strategies that experienced developers use to optimise their financial structures.

The key takeaways are clear: thorough preparation, solid documentation, and a strategic approach to negotiation are decisive. The common mistakes outlined above can all be avoided with proper planning and specialist advice at each stage of the process.

Land purchase financing should not be viewed simply as an obstacle to get past, but as a strategic tool that, when structured correctly, can significantly improve the profitability and viability of a real estate project.

In a competitive and constantly evolving market, staying current on financing trends and best practices is a genuine edge for developers who are serious about their results.

Planning your next real estate development or looking for financing to acquire land? Contact us today for a free initial assessment of your project. Our team will respond within 24 hours with a review of the financing options available for your specific situation.

Frequently Asked Questions

What percentage of financing can I expect for land purchase?

Financing percentages vary significantly depending on the type of land and the project. For consolidated urban plots you can typically obtain 60–80% of the appraised value, while for developable land this usually falls to 50–70%. Rural or undeveloped land rarely exceeds 50% financing. These percentages can improve with additional security or a strong credit history.

What are the main differences between financing developed and developable land?

Financing for fully serviced land generally offers better terms: higher LTV ratios, longer tenors, and more competitive interest rates. This reflects the lower perceived risk — infrastructure and utilities are already in place. Developable land, which requires additional investment for urbanisation, typically involves phased financing, more extensive documentation (urbanisation plans), and additional security to compensate for the higher risk profile.

How can I improve my chances of obtaining financing for land purchase?

To maximise your chances of approval, consider:

- Presenting a detailed business plan with rigorous market analysis.

- Demonstrating prior experience in comparable, successful projects.

- Contributing a meaningful equity deposit.

- Offering additional security beyond the land itself.

- Working with advisors who specialise in real estate financing.

- Providing thorough planning documentation that confirms the development is viable.

- Maintaining a clean credit record, both personal and corporate.

What alternatives exist if traditional banks reject my application?

If traditional bank financing is not available, consider:

- Private lenders specialising in real estate development.

- Professional real estate crowdfunding platforms.

- Negotiating a deferred payment arrangement directly with the seller.

- Bringing in equity partners in exchange for a share of profits.

- Real estate investment funds with a project financing division.

- Alternative lenders specialising in bridge loans.

- Blended structures that combine several smaller sources.