Business Credit Lines: A Guide to Flexible Financing

Business credit lines are flexible instruments that give companies quick access to capital for managing liquidity, funding projects, or covering unexpected costs. For any business looking to maintain financial stability and seize growth opportunities without tying up its immediate resources, this type of financing is essential.

A solid understanding of this financial tool is fundamental to sound decision-making — particularly in a business environment where speed of response can determine success or failure.

Business credit lines are key financing tools that allow companies to access capital flexibly and draw on funds precisely when needed.

In this article we look at what business credit lines are, how they work, their advantages over other financial products, and the requirements for obtaining one.

IMPORTANT NOTICE: The content of this article is for informational purposes only. The information provided does not constitute financial, legal, tax, or investment advice. The strategies, data, and figures on returns mentioned are estimates based on general market conditions and may vary significantly depending on the particular circumstances of each investor, property, location, and economic environment. The author and publisher of this content assume no responsibility for decisions that readers may make based on this information.

Table of Contents

- Definition and operation of business credit lines

- How to obtain a business line of credit

- Advantages of credit lines

- Differences between a loan and a credit line

- Conclusion and recommendations

- Resources and frequently asked questions

- Business credit lines give companies access to capital on demand, with interest charged only on the amount drawn.

- They are ideal for managing cash flow fluctuations and capitalising on unexpected business opportunities.

- Unlike loans, they offer flexibility in both drawdowns and repayments.

- They require a positive credit history and up-to-date financial documentation.

Definition and operation of business credit lines

A business credit line is a financial arrangement through which a bank makes a maximum amount of money available to a company for a set period. The key feature is that the company can draw on these funds in full or in part, according to its needs at any given time.

Unlike a traditional loan, a credit line works as follows:

- Interest is charged only on the capital actually drawn

- Once repaid, the credit becomes available to draw again — up to the agreed limit

- It offers greater flexibility on both timing and amounts

Practical usage examples:

- Inventory management: A retailer can finance additional stock purchases ahead of peak demand periods.

- Payment timing: A business can pay its suppliers before collecting from its own customers, avoiding cash flow pressure.

- Minor investments: Carrying out small refurbishments or purchasing equipment without committing large amounts of equity.

A credit line gives your company on-demand access to funds, helping you manage cash flow fluctuations, act on short-lived opportunities, or handle emergencies as they arise.

How to obtain a business line of credit

Applying for a business line of credit typically involves the following steps:

1. Needs assessment

Before starting any application, it is important to establish:

- The specific purpose for which the financing is needed

- The approximate amount required

- The company's repayment capacity

2. Collection of financial documentation

Financial institutions will typically ask for:

- Financial statements (balance sheet and profit and loss account)

- Credit history of the company and its principals

- Tax returns from recent financial years

- A business plan, particularly for newer companies

- Financial projections

3. Submission of the formal application

Once all documentation has been gathered, the application is submitted to the chosen financial institution along with the required supporting materials.

4. Credit analysis and assessment

The institution will carry out a thorough review covering:

- Financial solvency

- Revenue-generating capacity

- Credit history

- Sector-specific risk

5. Approval and formalisation

If the assessment is favourable, the specific terms will be agreed:

- Approved credit limit

- Applicable interest rates

- Opening, availability, or non-utilisation fees

- Term of the facility

- Any security requirements

Typical requirements for a business line of credit:

- Positive credit history, for both the company and its key directors

- Minimum trading history (typically 1 to 2 years of operation)

- Up-to-date financial statements showing positive results

- Security or collateral in certain cases, though smaller lines are sometimes granted without it

- Demonstrable tax and regulatory compliance

Approval of a business line of credit depends primarily on your company's financial strength, its credit history, and its ability to generate consistent cash flows.

Looking for flexible financing for your business? Contact us with no obligation. Our team will respond within 24 hours to assess the options available for your situation.

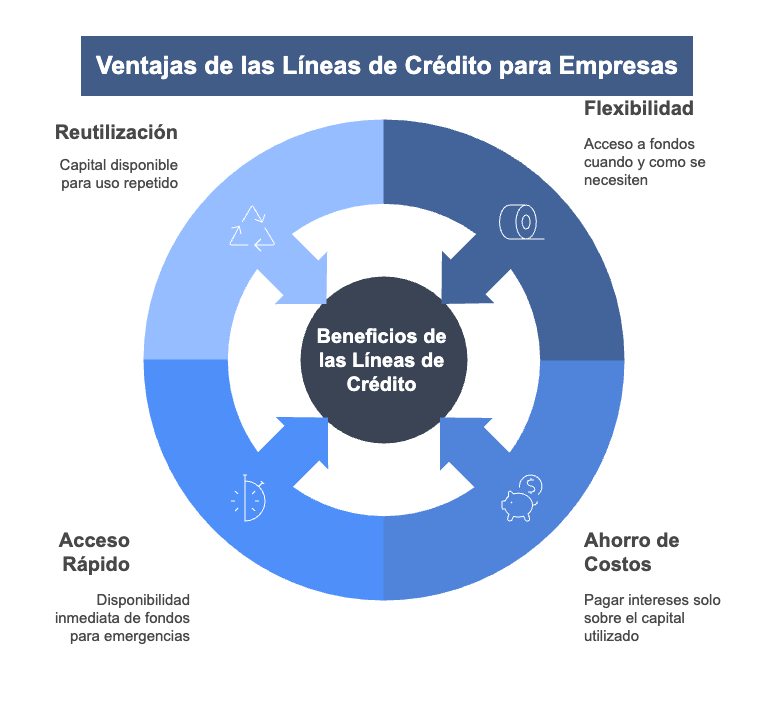

Advantages of credit lines

The advantages of credit lines for businesses are well-established, which explains why this instrument is among the most widely used by companies of all sizes:

Flexibility in accessing capital

The primary benefit is access to funds exactly when needed and in the precise amount required — without having to apply for additional financing each time a need arises.

Lower financial costs

Because interest is charged only on the capital drawn — not the total approved limit — financial costs are significantly lower than with a traditional loan.

Quick access to funds

Once a credit line is in place, funds are typically available immediately, which means:

- Rapid response to emergencies

- The ability to act on time-sensitive business opportunities

- Managing unexpected events without disrupting normal operations

Revolving availability

As drawn capital is repaid, it becomes available to use again — creating a revolving facility that provides ongoing financial flexibility and peace of mind.

Success story example:

A fashion retail chain spots an opportunity to buy a batch of seasonal products at a 40% discount following a supplier's closure. With its credit line in place, it can move immediately — without waiting to generate the necessary cash — and benefit from a significantly higher margin on those goods when they sell.

Credit lines let you draw funds as needed and pay interest only on what you use, unlike traditional loans, which require fixed repayments regardless of how much capital you are actually putting to work.

Differences between a loan and a credit line

Understanding the differences between a loan and a credit line is essential to choosing the right instrument for your company's needs:

| Feature | Business Loan | Business Credit Line |

|---|---|---|

| Amount and delivery | The full amount is advanced in a single payment | Access to a pre-agreed limit that can be drawn in full or in part |

| Payment method | Fixed periodic instalments on a defined schedule | Flexible repayments based on the capital used and the corresponding interest |

| Interest calculation | Applied on the total amount received | Charged only on the capital actually drawn |

| Duration | Fixed term until full repayment | Generally renewable (annual or indefinite) while conditions are maintained |

| Purpose | Usually tied to a specific purpose | Flexible use across various business needs |

| Reuse | Not reusable once repaid | Repaid capital becomes available again during the facility's life |

When to choose a loan?

- For significant investments with a clearly defined budget

- When a fixed sum is needed for a specific project

- For high-value acquisitions such as property or machinery

- When predictable fixed instalments are preferred for financial planning

When to choose a credit line?

- To manage cash flow fluctuations

- When flexibility in the use of funds is a priority

- To handle unexpected opportunities or emergencies

- When you want to minimise interest costs by paying only on what you use

The choice between a credit line and a loan ultimately depends on the nature of your financing need: flexibility versus structure, short term versus long term.

Conclusion and recommendations

Business credit lines are a highly valuable strategic tool that allows companies to stay liquid, respond to the unexpected, and seize opportunities quickly and efficiently. This article has covered their definition, operation, application process, competitive advantages, and how they compare to traditional loans.

The right choice of financing instrument should be based on a clear-eyed assessment of your company's specific needs:

- If you want flexibility and lower interest costs, a business credit line is probably the better option.

- If you need to finance a specific project with a defined budget, a traditional loan may be more appropriate.

- For many businesses, the optimal approach is to use both instruments in combination, matching each to the type of need it best serves.

Before applying for any financing:

- Assess your company's actual needs honestly

- Review your current and projected repayment capacity

- Compare the options available on the market

- Seek advice from a specialist financial adviser

Business credit lines are especially well-suited to companies with seasonal revenue cycles, those that need to manage working capital efficiently, or those that want to be ready to capitalise on opportunities at short notice.

When applying for a business line of credit, present complete and up-to-date financial documentation, maintain a positive credit history, and be prepared to demonstrate your company's ability to generate consistent cash flows.

Looking for a flexible financing solution or need to strengthen your working capital? Contact us today for a free initial assessment. Our team will respond within 24 hours with an evaluation of the financing options available for your specific situation.

Resources and frequently asked questions

Additional resources

To deepen your knowledge of business financing, we recommend:

- Private Financing for Businesses: Comparative Analysis with Traditional Banking

- Keys to Obtaining Financing for Your Business in Spain in 2025

- Complete Business Financing Guide: Options and Strategies for Growth

Frequently asked questions about business credit lines

What is the minimum and maximum amount available on a business credit line?

Amounts vary considerably depending on the institution, the size and age of the company, and its creditworthiness. Lines can range from as little as €10,000 to corporate facilities worth several million euros.

What documentation is required to apply for a credit line?

Generally, up-to-date financial statements, credit history, tax returns, a business plan, and in some cases security are required. The exact requirements may vary depending on the institution and the amount requested.

How long does approval take?

Timelines range from a few days for smaller lines with an existing banking relationship, to several weeks for larger amounts or new relationships. Thorough preparation of documentation can significantly speed up the process.

Are there penalties for cancelling a credit line early?

Some institutions may apply early cancellation fees, though this is less common than with loans. There may also be commitment fees on undrawn capital. Always review the specific contract terms carefully.

Business credit lines, used wisely, can make a meaningful difference to a company's growth and stability — providing the financial flexibility needed to thrive in an increasingly competitive business environment.