Bridge Loans for Real Estate Developers

Bridge loans for real estate developers have become an indispensable financial tool for development projects in Spain. This form of short-term financing lets developers act quickly on market opportunities, secure strategic plots and get projects moving while long-term financing is being arranged.

Unlike a traditional developer loan, bridge loans offer unmatched speed of approval and operational flexibility — qualities that can determine whether you seize an opportunity or lose it to a competitor. But using them effectively requires a clear understanding of how they work, what they cost and the risks involved.

This guide covers everything you need to know about bridge loans for developers: how they work, what lenders require, how to manage costs, and the strategies that maximise their value in today's competitive Spanish real estate market.

The financial conditions detailed in this post are indicative only and will vary depending on the lender, the borrower's profile, the specific characteristics of the transaction and prevailing market conditions. Nothing here constitutes a binding offer or guarantee of financing.

Table of Contents

- What are Bridge Loans for Real Estate Developers?

- Key Differences: Bridge Loan vs Developer Loan

- Advantages and Benefits of Bridge Financing

- Requirements and Conditions for Obtaining a Bridge Loan

- Costs and Financial Structure

- When to Use a Bridge Loan vs Traditional Financing

- Step-by-step Acquisition Process

- Exit Strategies and Refinancing

- Risks and How to Mitigate Them

- Frequently Asked Questions

What are Bridge Loans for Real Estate Developers?

A bridge loan for real estate developers is a short-term financing instrument designed to cover immediate capital needs while permanent long-term financing is being put in place. This type of bridge financing acts as a financial lifeline, allowing developers to start projects, acquire land or cover critical upfront costs without losing time.

Key Characteristics

Bridge loans for developers share these defining features:

- Short duration: Typically 12 to 24 months, rarely exceeding 36 months

- Fast approval: Decisions can be reached in as little as 2–3 weeks

- Operational flexibility: Terms structured around the specific needs of the project

- Defined purpose: To fund initial phases while a permanent developer loan is arranged

The primary role of these loans is to provide immediate liquidity for time-critical elements such as:

- Acquiring land in strategic locations

- Securing municipal licences and permits

- Covering upfront project costs and technical studies

- Breaking ground when market timing demands it

Key Points about Bridge Loans

✅ Speed of access: Capital available in weeks, not months

✅ Opportunity preservation: Avoid losing deals to slow bank processes

✅ Structural flexibility: Terms negotiated to fit the project

✅ Smooth transition: Facilitates a clean handoff to long-term financing

✅ Timing control: Lets the developer manage project milestones on their own schedule

Key Differences: Bridge Loan vs Developer Loan

Understanding the core differences between a bridge loan and a developer loan is essential for making sound financing decisions. Both serve the real estate sector, but their purposes, structures and ideal applications are quite different.

Detailed Comparison Table

| Aspect | Bridge Loan | Developer Loan |

|---|---|---|

| Duration | 12–24 months (maximum 36) | 2–4 years (until completion) |

| Purpose | Short-term transitional financing | Comprehensive project financing |

| Speed | 2–3 weeks | 2–4 months |

| Amount | Limited to immediate needs | 60–80% of total budget |

| LTV | 50–65% of value | 60–70% (up to 80% in favourable cases) |

| Timing | Project start / critical phases | Full project cycle |

| Guarantees | Land / specific assets | Mortgage over the entire project |

| Flexibility | High (negotiable terms) | Medium (more structured) |

When to Use Each

Bridge Loans — Best suited for:

- Land purchase opportunities with tight deadlines

- Starting projects before bank documentation is complete

- Taking advantage of favourable market conditions

- Short-term liquidity needs during permit or planning periods

Developer Loans — Best suited for:

- Projects with a long, well-planned construction programme

- Developments that need phased, certificate-linked financing

- Operations where cost is the priority over speed

- Projects with significant pre-sales already secured

For a fuller picture of traditional financing options, see our complete guide on developer loans.

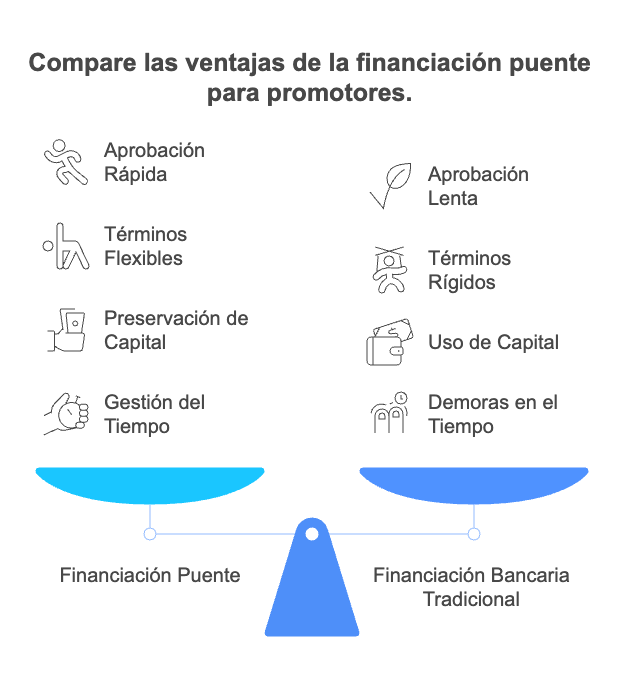

Advantages and Benefits of Bridge Financing

Bridge financing gives developers strategic advantages that can transform the competitiveness and pace of a real estate development. Here is what makes it valuable in practice.

1. Speed in a Competitive Market

The defining benefit of bridge loans is the ability to deploy capital quickly:

- Approval in 2–3 weeks versus 3–4 months for traditional bank financing

- Streamlined documentation focused on the specific project

- Decisive response from lenders who specialise in this space

This speed lets developers compete effectively in markets where good opportunities rarely wait.

2. Operational and Strategic Flexibility

Bridge loans offer a degree of adaptability that standard financing rarely matches:

- Terms tailored to the project's specific requirements

- Interest-only periods during construction

- Refinancing without punitive penalties when the time is right

- Drawdown schedules aligned with construction and sales timelines

3. Capital Preservation

Bridge financing lets the developer deploy equity more efficiently:

- Lower initial outlay compared with full self-funding

- Liquidity retained for other simultaneous opportunities

- Capital leveraged across a wider portfolio

- Capacity maintained to pursue multiple projects in parallel

4. Better Control of Project Timing

Bridge loans support more precise management of project milestones:

- Immediate start on permits, studies and site preparation

- Exploitation of favourable market windows before they close

- Synchronisation between project phases and financing schedules

- Reduced opportunity cost from delays

Requirements and Conditions for Obtaining a Bridge Loan

Securing a bridge loan for real estate developers means satisfying specific criteria that lenders use to assess and manage risk. Understanding these requirements will help you prepare a strong application and improve your chances of approval.

Developer Requirements

Experience and Track Record:

- Demonstrable history in comparable real estate projects

- Verifiable references from successfully completed schemes

- Sound financial standing of the developer, personally or corporately

- Technical capability within the team (architects, quantity surveyors, contractors)

Corporate Documentation:

- Articles of association and current powers of attorney

- Audited annual accounts for the last 3 financial years

- Up-to-date tax filings (corporate tax, VAT, income tax)

- Clean credit record with no significant defaults

Project-Specific Requirements

Technical and Legal Documentation:

- Clear title to the land or a binding purchase agreement

- Favourable planning certificate for the intended development

- Basic or full execution drawings certified by the relevant professional body

- Building permit obtained or in advanced processing

Commercial Viability:

- Detailed market study for the area and property type

- Business plan with realistic financial projections

- Competitor analysis and product positioning

- Sales strategy and pre-sales (where available)

Security Requirements

Lenders typically require:

- Mortgage over the land and future construction

- Personal guarantees from significant shareholders or directors

- Additional collateral (other properties, surety bonds) where applicable

- Specific insurance (all-risk construction, public liability)

Thinking about a bridge loan for your real estate project? Contact us for a free initial assessment. Our team will respond within 24 hours with a personalised evaluation of your options.

Costs and Financial Structure

The cost of a bridge loan for developers reflects both its short-term nature and the greater risk the lender takes on. A clear grasp of the cost structure is essential for assessing whether this financing makes economic sense for your project.

Interest Rate Structure

Bridge loans in Spain carry the following cost characteristics:

Indicative Rate Range (2025):

- Monthly rate: Between 1.0% and 1.2% per month (equivalent to 12–14% per annum)

- Risk adjustments: More complex projects may fall at the higher end of the range

- Pricing factors: Location, developer experience and quality of security offered

Components of Total Cost

Upfront Costs:

- Professional appraisal of the land and project

- Notary and land registry fees

- Arrangement fee (typically 1–2% of the loan amount)

- Management and technical study costs

Ongoing Costs:

- Interest on drawn capital only (not on the full facility)

- Monitoring and construction supervision fees

- Mandatory insurance (construction, public liability)

- Periodic administration costs

Exit Costs:

- Early repayment fee (if applicable)

- Novation or subrogation costs

- Costs associated with refinancing into permanent financing

Keeping Costs Under Control

To minimise the total financial burden:

- Negotiate interest-only periods: Defer capital repayment during construction

- Draw down in stages: Only take capital when you actually need it

- Plan the exit in advance: A clear refinancing strategy reduces last-minute costs

- Compare multiple lenders: Evaluate offers from several specialists simultaneously

When to Use a Bridge Loan vs Traditional Financing

Choosing between a bridge loan and traditional financing calls for a rigorous look at your project's circumstances and the current market. Each has a natural home.

When a Bridge Loan Makes Sense

Time Pressure in the Market:

- Land purchase opportunities with tight deadlines

- Favourable pricing conditions that won't last

- Competitive bidding for strategic assets

- Limited windows for breaking ground

Immediate Liquidity Needs:

- Starting a project before completing bank procedures

- Upfront costs such as permits, studies and licences

- Materials procurement under special pricing conditions

- Supplier payments with early-payment discounts

Portfolio Strategy:

- Running multiple projects in parallel

- Keeping liquidity free for new opportunities

- Efficient working capital management

- Avoiding long bank financing lead times

When Traditional Financing Is the Better Choice

Projects with Long Planning Horizons:

- Complex, multi-phase developments

- Schemes that require substantial pre-sales

- Projects where minimising financial cost is the top priority

- Operations with no time pressure whatsoever

If you are considering traditional options, our guide on whether a developer loan is the best fit for your project is worth reading.

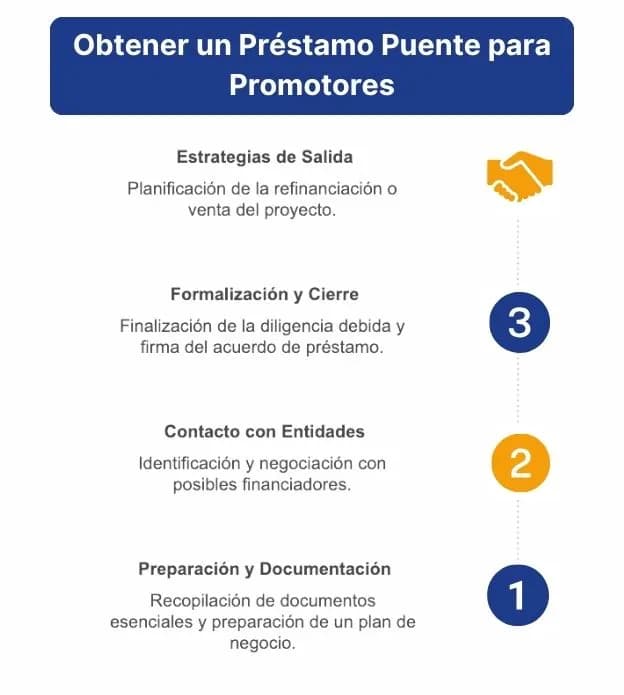

Step-by-step Acquisition Process

Getting a bridge loan for developers approved requires a structured approach. Thorough preparation at each stage is the biggest factor in securing good terms.

Phase 1: Preparation and Documentation (Week 1)

Document Gathering:

- Complete and up-to-date corporate documentation

- Financial statements for the last 3 financial years

- Technical project documentation (drawings, permits)

- Commercial and financial viability study

Dossier Preparation:

- Executive business plan (maximum 20 pages)

- Detailed project schedule and financing requirements

- Clearly defined exit strategy

- Risk analysis and mitigation measures

Phase 2: Lender Outreach (Week 2)

Selecting Lenders:

- Identify institutions that specialise in bridge loans

- Approach multiple lenders simultaneously

- Present the project and request indicative terms

- Carry out an initial assessment of fit and appetite

Initial Negotiation:

- Discuss headline terms (amount, duration, security)

- Clarify each lender's specific requirements

- Request binding offers with full conditions

- Compare proposals side by side

Phase 3: Closing (Week 3)

Final Due Diligence:

- Technical and legal review of the project by the lender

- Independent professional appraisal of land and assets

- Final documentation check and terms negotiation

- Agreement on definitive conditions

Signing:

- Loan agreement executed before a notary

- Mortgage security registered

- First drawdown released in line with agreed requirements

- Monitoring and oversight plan activated

Exit Strategies and Refinancing

A well-planned exit strategy is not optional — it is fundamental to the success of any bridge loan for developers, and lenders will scrutinise it closely before approving financing.

Main Exit Routes

1. Refinancing into a Developer Loan:

- Transition to long-term bank or private financing

- Access better terms once the project has progressed

- Retain an optimised security structure

- Significantly reduce ongoing financing costs

2. Sale of the Completed Project:

- Sell units individually as they complete

- Sell the whole project to an institutional investor

- Particularly effective in high-demand markets

- Full bridge loan repayment covered by sale proceeds

3. Mixed Refinancing:

- Combine partial unit sales with refinancing of the remainder

- Redeploy released capital into new projects

- Adapt flexibly to changing market conditions

- Reduce concentration risk across the portfolio

Recommended Exit Timeline

- Months 1–6: Advance the project and arrange permanent refinancing

- Months 6–12: Begin sales and/or close long-term financing

- Months 12–18: Execute the chosen exit strategy

- Contingency buffer: Keep an additional 6-month safety margin

GrupInversor's experience shows that projects with multiple, flexible exit routes secure better financing terms and carry lower operational risk.

Risks and How to Mitigate Them

Bridge loans for developers carry specific risks that require active management. Identifying and addressing these risks upfront is what protects the project — and the developer's balance sheet.

Key Risks

1. Refinancing Risk:

- Description: Difficulty securing permanent financing when the bridge matures

- Mitigation: Begin the developer loan process from day one

- Backup plan: Identify multiple refinancing lenders in advance

- Contingency: Pre-agree extension terms with the bridge lender

2. Market Risk:

- Description: Deterioration in values or sales conditions

- Mitigation: Conservative, up-to-date market research

- Diversification: Spread the portfolio across different locations

- Flexibility: Design the product to adapt if market conditions shift

3. Execution Risk:

- Description: Construction delays or cost overruns

- Mitigation: Detailed planning with contingency margins built in

- Control: Weekly monitoring of progress and budget

- Contracts: Fix-price agreements with financially sound contractors

Recommended Risk Management Strategies

Contingency Reserves:

- Maintain 15–20% of the project budget as a liquid reserve

- Keep uncommitted credit lines available

- Have the capacity to inject additional equity if needed

Risk Diversification:

- Limit exposure to any single project to below 60% of total capital

- Stagger projects over time to reduce peak exposure

- Diversify by market and asset type in line with your experience

For a deeper look at risk management in real estate, see our article on how to mitigate risk in real estate flipping operations.

Conclusion

Bridge loans for real estate developers are a strategic financial instrument that can sharpen any developer's competitive edge. Their value lies in the speed at which capital can be accessed and the flexibility they provide — two qualities that matter greatly in today's fast-moving real estate market.

Success with bridge financing comes down to three things: a meticulous exit strategy, a realistic assessment of costs and risks, and the right specialist lender who understands how real estate development actually works.

At GrupInversor, with over 20 years of experience in real estate financing, we have seen that developers who structure their bridge loans well do more than just respond to opportunities faster — they improve overall profitability by cutting opportunity costs and accelerating development cycles.

The choice between a bridge loan and traditional financing must be made case by case, weighing the project's specific circumstances, market conditions and the developer's strategic goals. The right advice at that decision point can make the difference between a profitable deal and a missed one.

Do you have a real estate project that needs fast financing? Contact us for a personalised assessment. Our team will respond within 24 hours with a recommendation on the best bridge loan options for your situation.

Frequently Asked Questions

What is the main difference between a bridge loan and a developer loan?

The key difference lies in purpose and timeframe. A bridge loan is temporary financing (12–24 months) designed to cover immediate needs while permanent financing is arranged. A developer loan is comprehensive, long-term financing (2–4 years) covering the full project cycle. Bridge loans stand out for fast approval (2–3 weeks versus 2–4 months) and their focus on unlocking liquidity quickly — whether to start a project or capture a market opportunity.

How long does it take to obtain a bridge loan for developers?

The typical process takes 2–3 weeks — substantially faster than traditional bank financing. The timeline breaks down as follows: Week 1 — prepare documentation and project dossier; Week 2 — contact lenders, present the project and negotiate terms; Week 3 — final due diligence, signing and first drawdown. Hitting that timeline requires having all documents ready and working with lenders who specialise in this type of financing.

What guarantees are required for a real estate bridge loan?

Standard security includes: a mortgage over the land and future construction as the primary guarantee, personal guarantees from significant shareholders or directors, mandatory insurance (all-risk construction, public liability), and in some cases additional security such as other properties or surety bonds. The lender also needs a clearly defined exit strategy — sale or refinancing — that demonstrates a credible path to repayment. The value of the security must be proportionate to the risk the lender is taking on.

What are the typical costs of a bridge loan for developers in Spain?

For 2025, indicative costs include: interest rates between 1.0%–1.2% per month (12–14% per annum), an arrangement fee of 1–2% of the loan amount, closing costs (appraisal, notary, registration), mandatory insurance for the duration and monitoring fees. While rates are higher than traditional financing, the short term and operational flexibility can justify the premium for projects where speed is essential.

When is it advisable to choose a bridge loan over traditional financing?

A bridge loan is the right choice when: there is genuine time pressure to capture a market opportunity (land purchase with a tight deadline, attractive pricing that won't last); immediate liquidity is needed for critical early costs (permits, studies, groundworks); you need to move independently of slow bank approval cycles; you are managing a portfolio of simultaneous projects; or you need flexibility that traditional financing cannot provide. Standard financing is more appropriate when timing is not a concern, cost is the overriding priority, or the project has long, complex phases.

What exit strategies exist for a bridge loan?

The main exit routes are: refinancing into a traditional developer loan once the project has advanced and the documentation is bank-ready; selling the completed project, either unit by unit or as a whole to an institutional buyer; or a hybrid approach combining partial sales with refinancing of the remaining balance. The exit strategy must be defined before signing and communicated clearly to the lender. Projects with multiple viable exit options consistently achieve better financing terms and carry lower risk.