Private Financing for Businesses: A Comparative Analysis with Traditional Banking

Private financing for businesses has emerged as a powerful and flexible alternative for companies of all sizes — particularly for growing businesses or those with specific needs that traditional banking cannot always meet.

Today's financial landscape is far more diverse and competitive than it used to be, which means businesses no longer have to rely exclusively on banks to access capital.

Unlike bank financing, which tends to follow standardised processes and relatively rigid criteria, private options offer a genuinely different approach that many business owners and CFOs find more practical. Understanding the key differences between the two models is essential for making sound financial decisions.

In this article, we take a close look at the differences between bank and private financing, examine the advantages of private financing, and help you determine when to choose private financing based on your company's specific circumstances.

IMPORTANT NOTICE: The information provided in this article is for informational purposes only and does not constitute financial advice. Specific financing conditions vary according to each company's situation, the sector it operates in, its credit history, and market conditions. We recommend consulting with a financial specialist for personalised guidance.

Table of Contents

- Definition and Contextualization

- Comparison: Bank Financing vs. Private Financing

- Advantages of Private Financing

- When to Choose Private Financing

- Conclusions and Recommendations

- Frequently Asked Questions

KEY POINTS:

- Private financing offers greater flexibility and speed than traditional bank lending.

- Approval processes are typically faster in private financing.

- A range of private financing structures exists to suit different sectors and needs.

- The choice between bank and private financing should reflect your business's specific circumstances.

- The two approaches can be combined to build an optimised financial structure.

Definition and Contextualization

Bank Financing for Businesses

Bank financing for businesses is the traditional model for raising external capital. It is characterised by standardised processes that involve a thorough review of the company's credit history, set documentary requirements, and — in most cases — a demand for substantial security.

Products in this category include:

- Short-, medium-, and long-term loans

- Credit lines and revolving credit facilities

- Invoice discounting and factoring

- Leasing and renting

Banks apply relatively rigid evaluation criteria, which can make access difficult for younger companies, businesses with innovative models, or those operating in emerging sectors. As we explored in our article on keys to obtaining financing for your business in Spain, meeting the requirements for bank financing is something many businesses struggle with.

Private Financing for Businesses

Private financing for businesses covers a range of non-bank alternatives that provide capital on generally more flexible terms. This ecosystem includes:

- Private debt funds (direct lending)

- Peer-to-peer lending platforms (P2P)

- Sale and leaseback financing

- Venture capital and private equity funds

- Family offices and private investor groups

These options stand out for their ability to adapt to each company's specific needs and for offering faster processes — though they may involve different trade-offs in terms of cost, governance, and requirements. Our complete guide to business financing explores the full range of alternatives available in today's market.

Comparison: Bank Financing vs. Private Financing

Understanding the differences between bank and private financing is essential for shaping a sound financial strategy. Below we look at the main areas where the two approaches diverge.

Access to Financing

Bank Financing:

- Standardised, inflexible evaluation criteria

- Strong focus on credit history and security

- More challenging for young or innovative companies

- Structured, documentation-heavy assessment processes

Private Financing:

- More receptive to innovative or disruptive projects

- A more holistic view of business potential

- Accessible to companies with higher-risk profiles

- Individually tailored evaluation based on the project itself

Where traditional banks focus primarily on historical financials and tangible security, private financiers typically also consider future growth potential, the quality of the business model, and the strength of the management team — broadening access for businesses that might not pass a standard bank screen.

Speed and Agility in Approval

Bank Financing:

- Slower, more bureaucratic processes

- Multiple levels of internal sign-off

- Extensive documentation and formal requirements

- Longer typical approval timelines

Private Financing:

- Leaner, more direct processes

- Less administrative overhead

- Faster decision-making

- Well suited to situations requiring a quick response

Speed is one of the most tangible advantages of private financing — particularly valuable for businesses that need to act on a market opportunity or address an urgent situation.

Requirements and Guarantees Required

Bank Financing:

- Standard requirement for real estate or personal guarantees

- Extensive, standardised documentary requirements

- Assessment focused on conventional financial ratios

- Limited flexibility for unusual circumstances

Private Financing:

- Greater flexibility in how security is structured

- Non-conventional assets can be accepted as backing

- Qualitative business factors taken into account

- Adapted to the specific circumstances of each borrower

While banks typically require conventional collateral such as property or personal guarantees, private financiers can work with more creative structures — or base their decision on business assets such as intellectual property, contracted revenues, or the value of the client base.

Financial Costs and Terms

Bank Financing:

- More standardised pricing

- Limited room to negotiate terms

- Relatively rigid cost structure

- Predefined tenors by product category

Private Financing:

- Terms adaptable to each project

- Greater scope for negotiation

- Flexible repayment and maturity structures

- Ability to align amortisation with business cash flows

Private financing tends to carry a higher cost, but offers the ability to structure terms around the operational reality of each business — including repayment profiles that match the company's cash generation cycle.

In some cases, private financing is the only viable option — for businesses with adverse credit events, listings in bad debt registers (e.g. CIRBE, RAI, ASNEF), high existing debt levels, or other factors that rule out traditional bank lending.

Want to understand which type of financing best fits your company? Contact us and we will advise you on the most suitable options for your specific situation.

Advantages of Private Financing

Private financing for businesses offers a number of significant advantages that explain its growing adoption across the business community.

Flexibility in Conditions and Negotiation

One of the most important advantages of private financing is the ability to structure genuinely tailored agreements. Unlike standardised bank products, private financing can be designed to reflect:

- Grace periods aligned with the business development cycle

- Repayment schedules matched to expected cash flows

- Multi-tranche structures with different characteristics at each stage

- Hybrid financing structures combining debt and equity elements

This flexibility makes it possible to build financial solutions that truly reflect the operational and strategic reality of each company. A clear example is construction and real estate development, where products such as developer loans or property flipping financing can be structured with repayments tied to project milestones.

Faster Approval Processes

Reduced bureaucracy and direct decision-making are hallmarks of private financing:

- Faster project assessment

- Significantly shorter response times

- More streamlined due diligence

- Fewer intermediaries involved

This speed is particularly valuable for businesses that need to fund a growth opportunity quickly or respond to an urgent operational challenge.

Variety of Financing Options

The private financing ecosystem offers a broad range of solutions, allowing businesses to find the structure that best fits their needs:

- Dedicated financing for business acquisitions

- Tailored solutions for restructuring situations

- Sector-specific instruments (technology, real estate, industrial)

- Options adapted to different stages of business development

As outlined in our sector-specific financing overview, each form of private financing can be shaped around specific business objectives.

Access in Difficult Circumstances

Private financing offers solutions for businesses in situations that traditional banks would typically decline:

- Companies with adverse credit events or listings in bad debt registers

- Businesses with financial structures undergoing improvement

- Operations going through an active restructuring

- Companies with an urgent capital requirement

- Projects in emerging sectors with few comparable precedents

This ability to accommodate difficult circumstances makes private financing a genuine option when conventional sources are not.

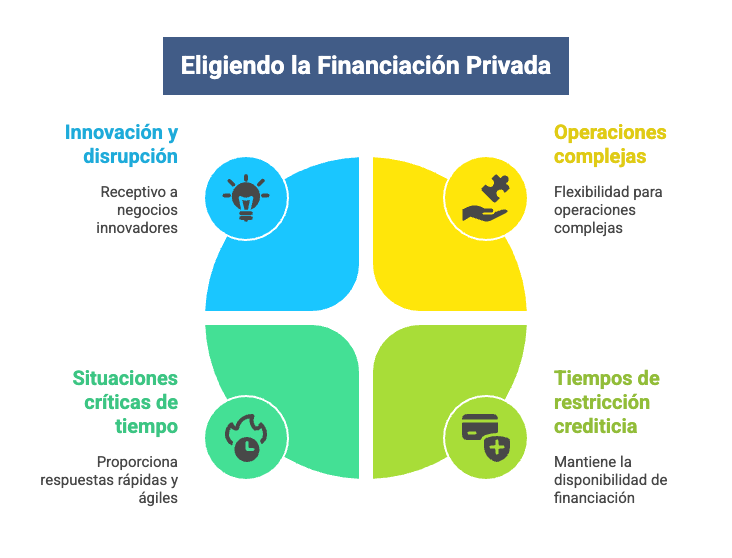

When to Choose Private Financing

The right time to choose private financing depends on your company's specific situation and objectives. The following scenarios are the most common cases where private financing is the better fit.

For Innovative or Disruptive Projects

Companies pursuing innovative business models or disruptive technology often find private financiers more receptive than banks:

- Startups in rapid growth phases

- Businesses developing emerging technologies

- Models that are scalable but not yet proven at scale

- Projects requiring significant upfront investment before revenues arrive

Private financiers are generally better equipped to evaluate innovation and disruption potential, rather than relying solely on conventional financial metrics.

When Speed is Critical

Some business situations are genuinely time-sensitive, and the ability to move quickly can make all the difference:

- Acquisition opportunities with tight deadlines

- Urgent liquidity needs

- Market expansion windows that won't stay open long

- Rapid competitive shifts requiring an immediate response

When time is a critical factor, private financing is typically the better option.

For Complex Operations

Financially complex transactions often benefit from the structuring flexibility that private financing provides:

- Corporate acquisitions (M&A)

- Expansion into multiple international markets

- Restructurings involving several business units

- Projects combining different asset classes or business lines

The ability to design bespoke solutions allows these transactions to be handled more efficiently than standardised bank products allow.

During Periods of Credit Restriction

When banks tighten their lending criteria, private financing tends to remain available:

- During unfavourable macroeconomic conditions

- Through banking sector consolidation periods

- When regulatory changes affect credit availability

- For sectors temporarily hit by cyclical uncertainty

Maintaining access to private financing sources reduces dependence on bank credit cycles — an important form of financial resilience.

For a full comparison of options and how to select the right one, see our complete guide to business financing options.

Conclusions and Recommendations

The choice between bank financing and private financing should be based on a detailed analysis of your organisation's specific needs — taking into account urgency, transaction complexity, risk profile, and strategic objectives.

Private financing stands out for its flexibility, speed, and ability to adapt to a wide range of business situations. That said, the specific cost and structural implications need to be considered carefully before committing.

To make the most informed decision, we recommend:

-

Assess your financing needs thoroughly — not just in quantitative terms, but qualitatively as well

-

Compare alternatives across both banking and private channels — looking at not just cost but terms, flexibility, and overall fit

-

Consider combining both approaches to build an optimised overall financial structure

-

Work with specialist advisers who can identify the most suitable options for your specific situation

-

Evaluate strategic fit — consider how each option aligns with the medium and long-term direction of your business

Choosing the right financing strategy is one of the most important decisions in any business's development. The differences between bank and private financing are, in practice, opportunities to design a capital structure that genuinely serves the needs of your organisation.

Not sure which financing model is right for your business? Contact us for personalised advice on the best options for your situation.

Frequently Asked Questions

What are the main differences between bank financing and private financing?

The key differences lie in flexibility, approval speed, security requirements, and implementation timelines. Bank financing is more standardised and subject to tighter criteria, while private financing is more adaptable to the specific needs of each company — though with potentially different implications for cost and structure.

What advantages does private financing offer over bank lending?

The main advantages include: greater flexibility in structuring terms, faster approval processes, a broader view of what constitutes a viable project, the ability to finance complex or bespoke transactions, and access to capital in situations where traditional banking would not lend. Private financing enables genuinely tailored solutions rather than off-the-shelf products.

In what situations should I consider private financing as a first option?

Private financing is likely the right choice when: you need a fast response to seize a market opportunity, your business has an innovative or disruptive profile that banks struggle to assess, you need a complex or customised financial structure, you are financing an expansion or acquisition with specific characteristics, or when traditional bank lending is not available to your sector or company.

Can both approaches be combined to optimise a company's financial structure?

Absolutely. Many businesses use mixed strategies that draw on the strengths of both approaches depending on the specific need. For example, bank financing for routine or long-term requirements, and private financing for more complex projects or situations requiring greater speed. This diversification also reduces dependence on a single source of capital and strengthens your overall negotiating position.